- English

- عربي

Game playing or the start of a no-deal?

Sterling traders have taken a strong dislike (finally) to this uncertainty and hit GBP hard.

We had questioned very recently if the market was too complacent over a Brexit trade deal and within days, investors have woken up to pricing in much more Brexit risk premium. After ignoring the lack of progress in talks in recent months, the pound has weakened sharply pushing cable towards 1.28 and EUR/GBP above the June high of 0.9176 (albeit also on the back of a surprisingly less dovish ECB Meeting) as the EU threatened legal action over the UK plans to tear up the Withdrawal Agreement. The trade-weighted GBP has fallen over 2% from its recent peak.

What is the Internal Market Bill?

State aid is the major dividing issue in Brexit negotiations and the UK government is keen to keep a free hand to support its own industries once the transition period ends this year. On the flip side, the EU wants some form of oversight to ensure its firms are not at a disadvantage. However, last year’s Withdrawal Agreement bound the UK to still follow certain EU state aid rules, which may especially affect trade between Northern Ireland and the EU.

The proposed new UK Bill looks to ignore this and would allow ministers to circumvent state aid provisions contained within the Irish backstop. It would ensure companies in Northern Ireland have ‘unfettered access’ to the UK internal market ensuring the unity of the single UK market in the event of a no-deal outcome to trade negotiations. However, the UK admits this breaks international law in a “specific and limited way” and the bill has dramatically undermined the trust between both sides, making it even harder to reach a last-minute compromise trade deal.

Downside Playbook

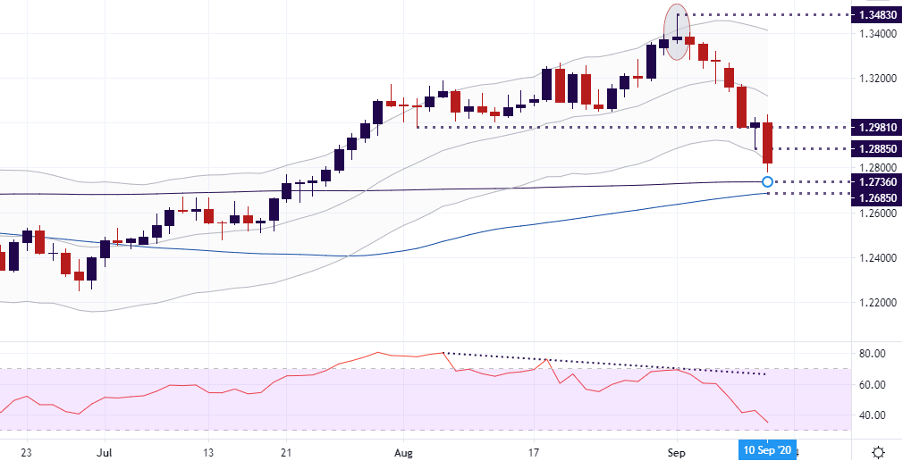

Risks to sterling remain heavily skewed to the downside in the near-term with strong bearish momentum seen over the last few sessions after prices topped out with an inverted hammer or shooting star candle at the start of this month. Bearish divergence between that spike high and the RSI was also significant.

Today’s selloff is the biggest since the height of the pandemic in March and cable has busted through the August low and support at 1.2981, which now acts as resistance to any move higher. The sharp move today through yesterday’s low at 1.2885 has re-established the bear run from the longer-term 1.35 high which means we may now test lower levels around the 1.2650/00 zone. Before this, prices will have to test support at 1.2736 (200-day Moving Average) ahead of the 100-day MA at 1.2685.

The EU has now given the UK three weeks to back down from its plans and warned that it jeopardises any efforts for a trade agreement. Markets await the conclusion of the EU’s Barnier – UK’s Frost talks which conclude this week, but traders are not looking back and fearing the worst.

Upside Playbook

The EU has not yet suspended negotiations and the view in Dublin is that the strident nature of the UK’s new legislation is most likely ‘sabre-rattling’. Indeed, the UK government has presented the Bill as a safety net in case trade negotiations fail. Is this a game of chicken with the first hand played by the UK, as the clock ticks down to the de facto mid-October deadline?

Resistance above lies at Wednesday’s low at 1.2885 and then the August low at 1.2981. Cable would need to close above here to arrest the very strong downside momentum.

Ready to trade?

It's quick and easy to get started. Apply in minutes with our simple application process.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients. Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.