- English

- عربي

March 2026 US Employment Report: Chunky Headline Beat But Geopolitical Uncertainty Presents Downside Risks

Payrolls Top The Forecast Range

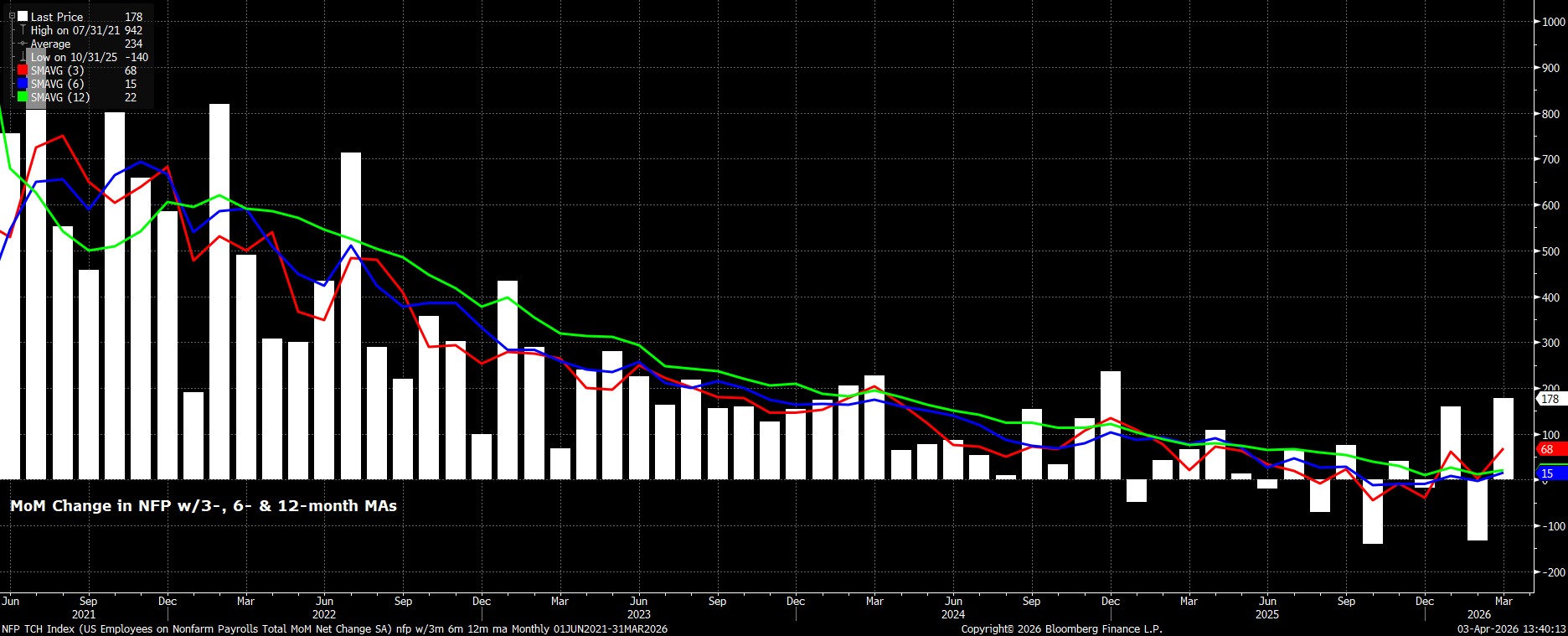

Headline nonfarm payrolls rose by +178k last month, well above not only consensus expectations but also outside the typically wide forecast range of -15k to +150k. Still, one must recall that the headline payrolls print is likely overstating job gains to the tune of as much as 60k per month, necessitating a degree of caution in interpreting the figures.

Along with the March print, the prior two payrolls figures were revised by a net -7k, marginal in the grand scheme of things, subsequently taking the 3-month average of job gains to +68k, just a touch above the breakeven rate.

Digging Into The Details

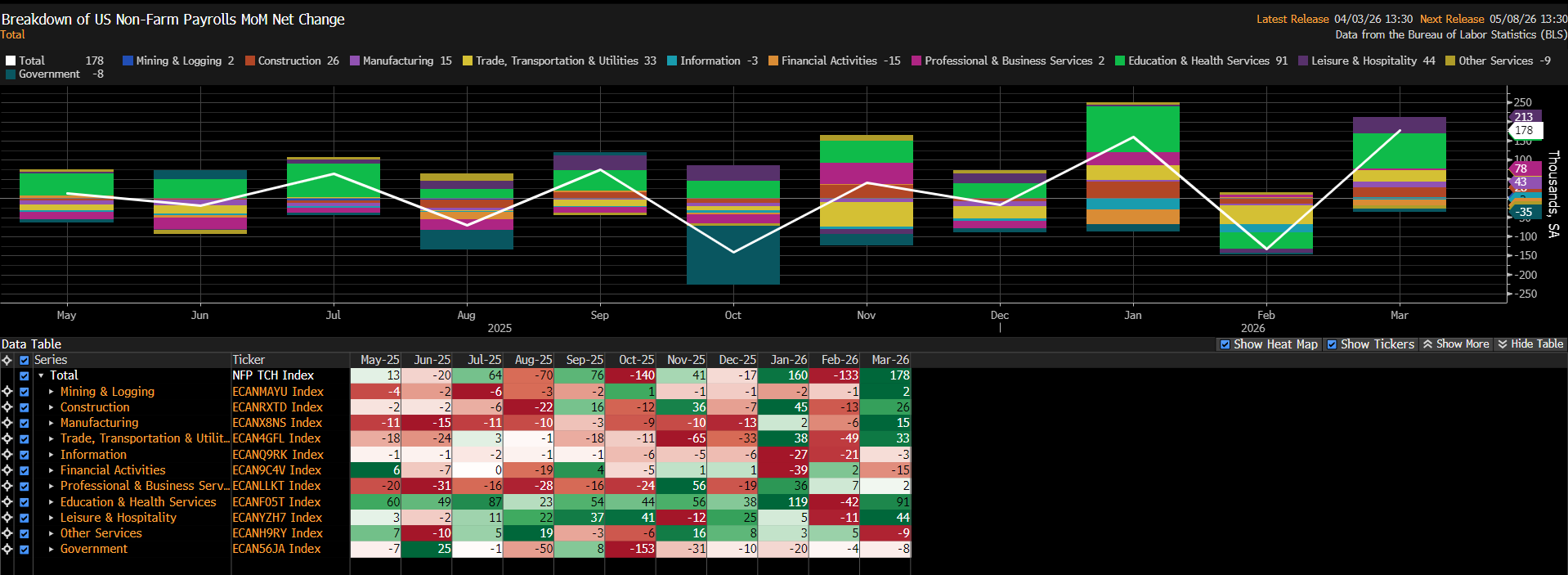

Under the surface, the sectoral split of job gains pointed to the sizeable payrolls beat stemming from broad-based job gains. Once again, Healthcare continues to prop things up, adding 91k jobs on the month, while Leisure & Hospitality was another key contributor once more. The much warmer weather seen in March also saw a notable rebound in weather-sensitive sectors such as Construction and Manufacturing.

Earnings Growth Stays In Check

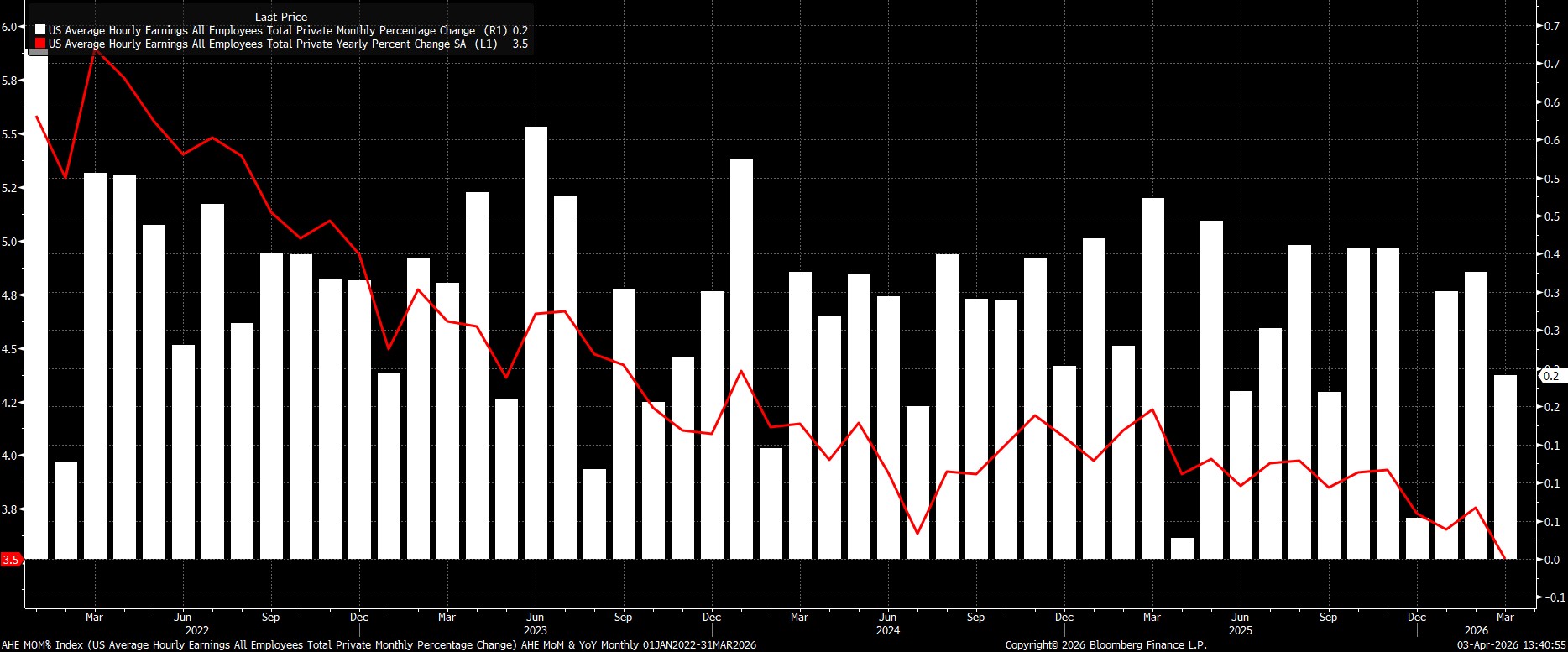

Sticking with the establishment survey, the report pointed to pay pressures remaining relatively contained, with average hourly earnings having risen by 0.2% MoM last month, in turn taking the annual pace of earnings growth to 3.5% YoY.

That said, while such a pace of earnings growth presents little by way of concern in terms of upside inflation risks, those risks are clearly present in the short-term, given ongoing conflict in the Middle East, and the subsequent surge in energy prices. The potential for second-round effects, though, given the margin of labour market slack that is present, is considerably lower than around the time of the last major energy shock in 2022, meaning that the FOMC should be able to ‘look through’ any energy-induced rise in headline inflation for the time being.

Household Survey Also Robust

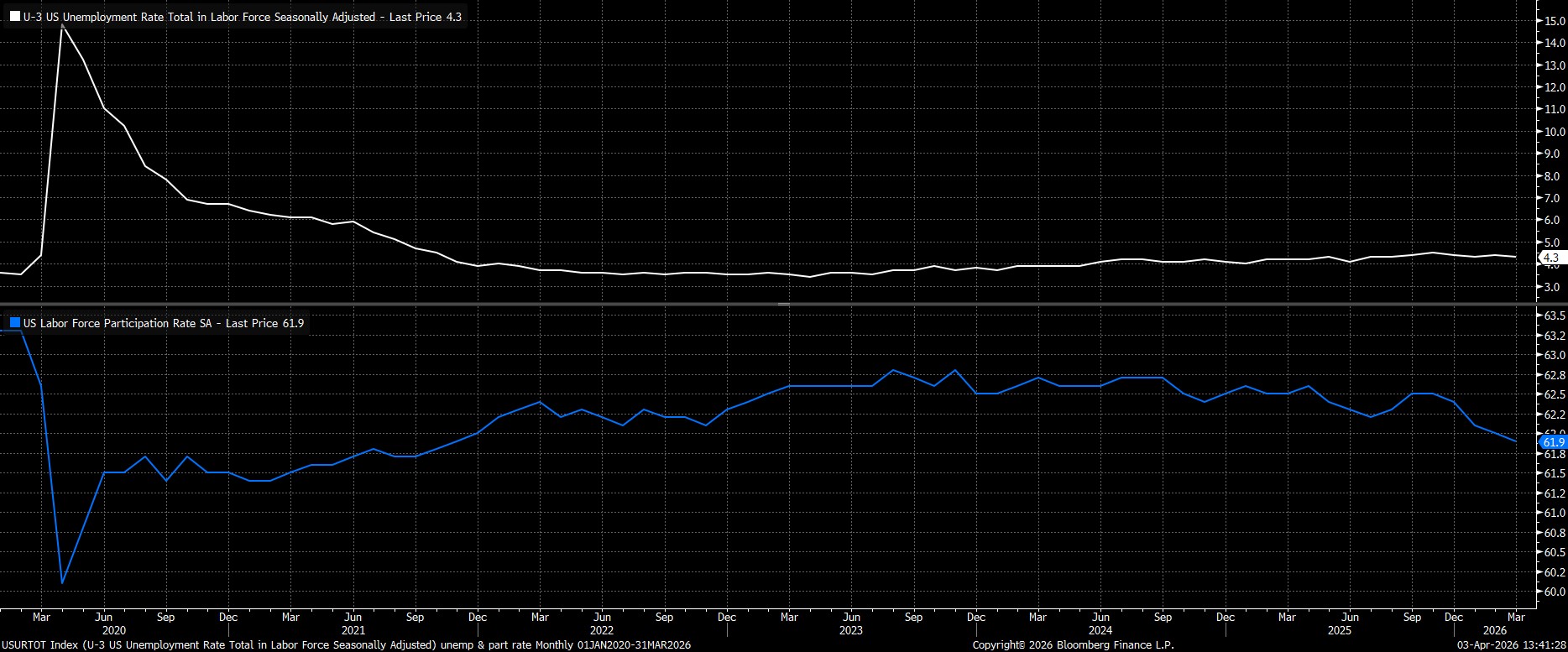

Turning to the household survey, the jobs report pointed to unemployment having surprisingly dipped 0.1pp to 4.3% last month, though this was largely down to the labour force having shrunk, with participation declining to a cycle low 61.9%.

While the household survey is also far from perfect, given the BLS’ issues in adapting to the rapidly changing size and composition of the labour force, it nonetheless carries greater weight from a policy perspective, considering the present focus on the potential – or lack of – for higher energy prices to be a catalyst for second-round inflation effects, as outlined above.

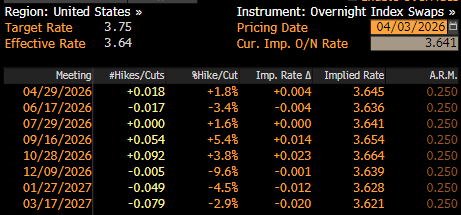

Money Markets Reprice Hawkishly

In reaction to the data, money markets repriced marginally in a hawkish direction, albeit in very, very thin conditions. The USD OIS curve, at the time of writing, now prices no action at all from the Fed this year, compared to the 5bp of easing that was discounted pre-release.

Conclusion

Taking a step back, the March jobs report seems unlikely to significantly alter the near-term Fed policy outlook.

As Chair Powell outlined earlier this week, the FOMC’s current policy stance leaves them in a ‘good place’ to ‘wait and see’ how the economic outlook evolves. While the labour market remains somewhat fragile under the surface, and arguably could do with greater policy support, the FOMC will stand pat for the time being, until the magnitude and duration of the energy price shock, and its impact on headline inflation, becomes clearer.

Providing that the ‘fog of war’ does indeed lift, however, and that any energy-induced uptick in headline inflation does prove temporary, as I’d expect it to, then further rate reductions, to provide additional support to the employment backdrop, are likely still on the cards later in the year. While the March jobs report was a notable upside surprise, it’s reasonable to expect that higher energy prices, and the incoming negative demand shock, both post significant downside risks to the employment objective. These cuts, though, are unlikely to come before H2, and not until Chair designate Warsh has formally taken the helm.

Money markets, to my mind, continue to price too hawkish a policy path, assuming a linear relationship along the lines of ‘higher energy prices = higher inflation = higher rates’, forgetting not only the likely temporary nature of that higher headline inflation, but also the employment side of the dual mandate, where further deterioration would likely be the trigger for the FOMC to act once more.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients. Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.