- English

- عربي

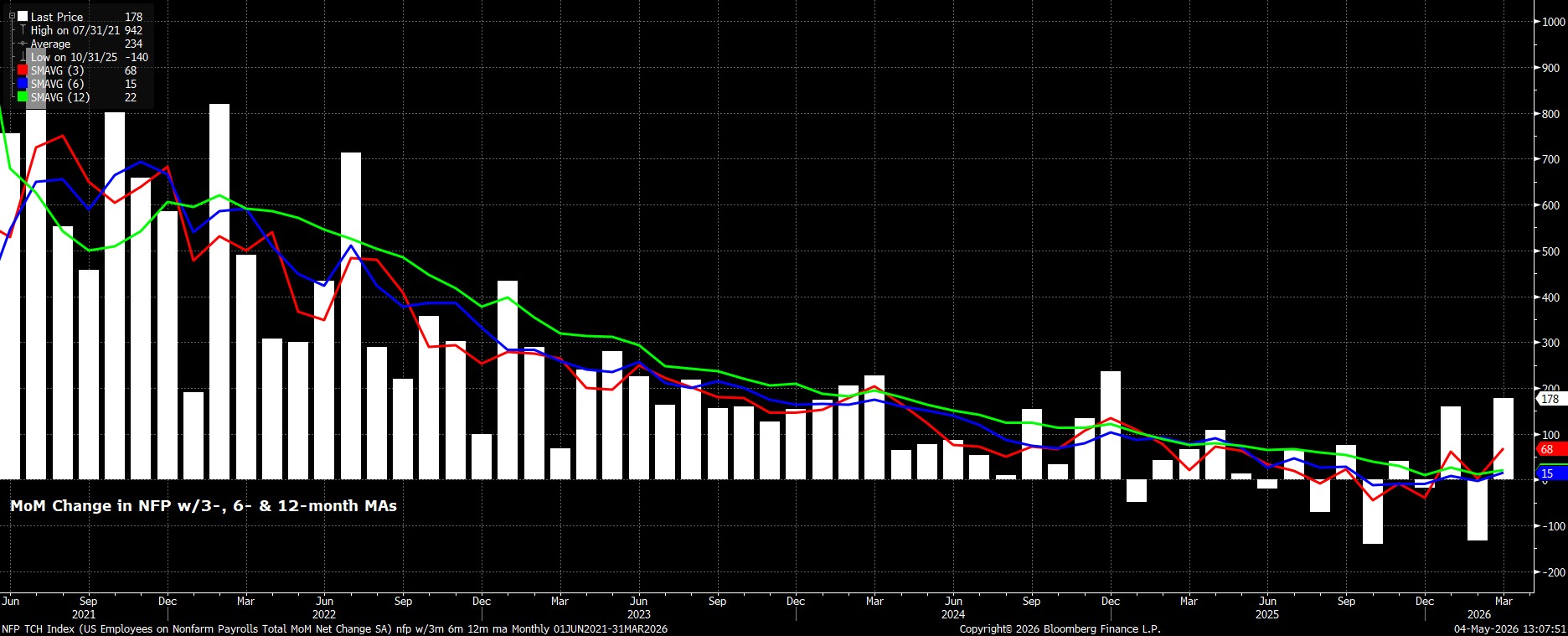

Payrolls Growth To Slow

Headline nonfarm payrolls are set to have risen +65k last month, a fairly substantial slowdown from the +178k increase seen in March, albeit a rate that would be broadly in line with the 3-month moving average of job gains, which presently stands at +68k. Furthermore, a print in line with consensus would likely remain north of the breakeven pace of job creation, which is likely around zero, even accounting for the headline NFP figure likely continuing to overstate ‘actual’ job creation by some margin.

In any case, the range of estimates for the payrolls print is as wide as ever, from -15k to +140k, though it is important to recall that in an economy with such a low breakeven rate, not only are significant month-to-month swings in job creation more likely, but also that a substantial payrolls decline could be seen in any given month, even if economic growth were running at its potential level. Put another way, a big negative NFP print shouldn’t be as ‘scary’ as it once might’ve been.

March Boosts To Become A Drag

Last time out, headline payrolls growth was boosted by a number of one-off factors. These include the end of strike action in the Healthcare sector, considerably better weather than in February providing a tailwind to Construction, and a concurrent lift to employment in Leisure & Hospitality for the same reason. All three of those factors which added to headline payrolls last time out are, at a minimum, unlikely to repeat in April, thus acting as something of a drag on overall employment growth.

Meanwhile, one must also recall that the March survey week came too early in the month to reflect any impact of developments in the Middle East, either in terms of the damage caused by higher energy and input prices, or so far as broader economic uncertainty may have started to dent labour demand. The April report should shed greater light on both of these factors however, thus far, there appears to have been little detrimental impact from geopolitical events on what remains a robust US economy.

Leading Indicators Paint A Rosy Picture

As for leading indicators for the payrolls print, the picture is generally a rosy one. The ADP weekly employment indicator pointed to an average of 39.25k jobs having been added per week in the 4 weeks ending just prior to the survey week, which would in turn point to private sector jobs having increased approx. +157k over that period.

Meanwhile, jobless claims have remained at historically low levels. Although initial claims actually rose by 10k between the March and April reference weeks, last week’s initial claims print, at 189k, was the lowest such figure since the late-60s. Continuing claims, meanwhile, have also continued on a steady path lower, falling to a 2-year trough in the April NFP reference week.

The only slight blot on this particular copybook comes from the ISM manufacturing survey, where the employment sub-index fell to a YTD low 46.4 last month; as of the time of writing the ISM services survey has yet to be released.

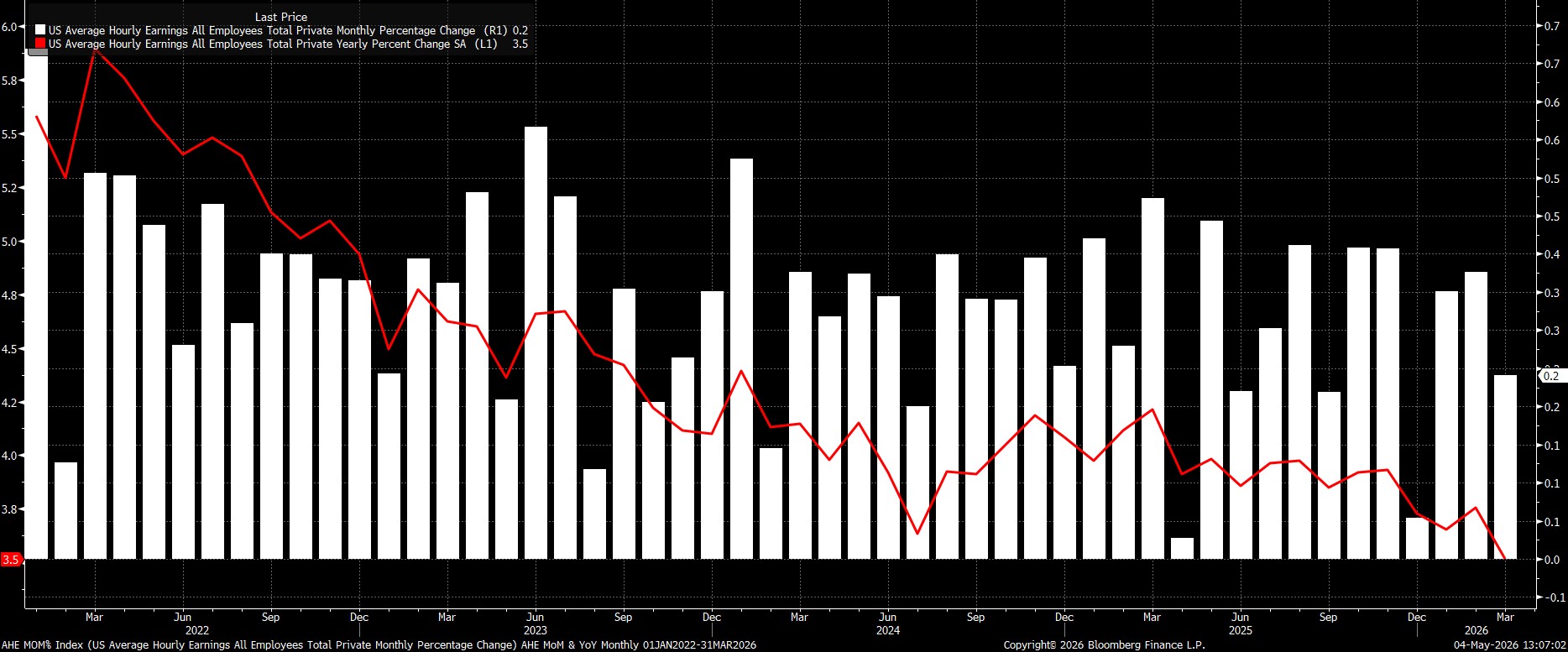

Earnings Growth To Remain Tepid

Sticking with the establishment survey, data is set to show earnings growth remaining relatively contained, at 0.3% MoM, just 0.1pp quicker than the pace seen last time out. While such a print would drag the annual pace of earnings growth to 3.8% YoY, from a prior 3.5% YoY, this to a significant degree reflects a base effect from last April, and is unlikely to be of particular concern.

In fact, earnings growth in general continues to run at a pace that is broadly consistent with achievement of the FOMC’s 2% inflation aim over the medium-term. Still, though the labour market may not pose upside inflation risks at the current time, those risks are clearly present, particularly as the impact of higher energy prices and supply chain disruption stemming from conflict in the Middle East becomes clearer over coming months.

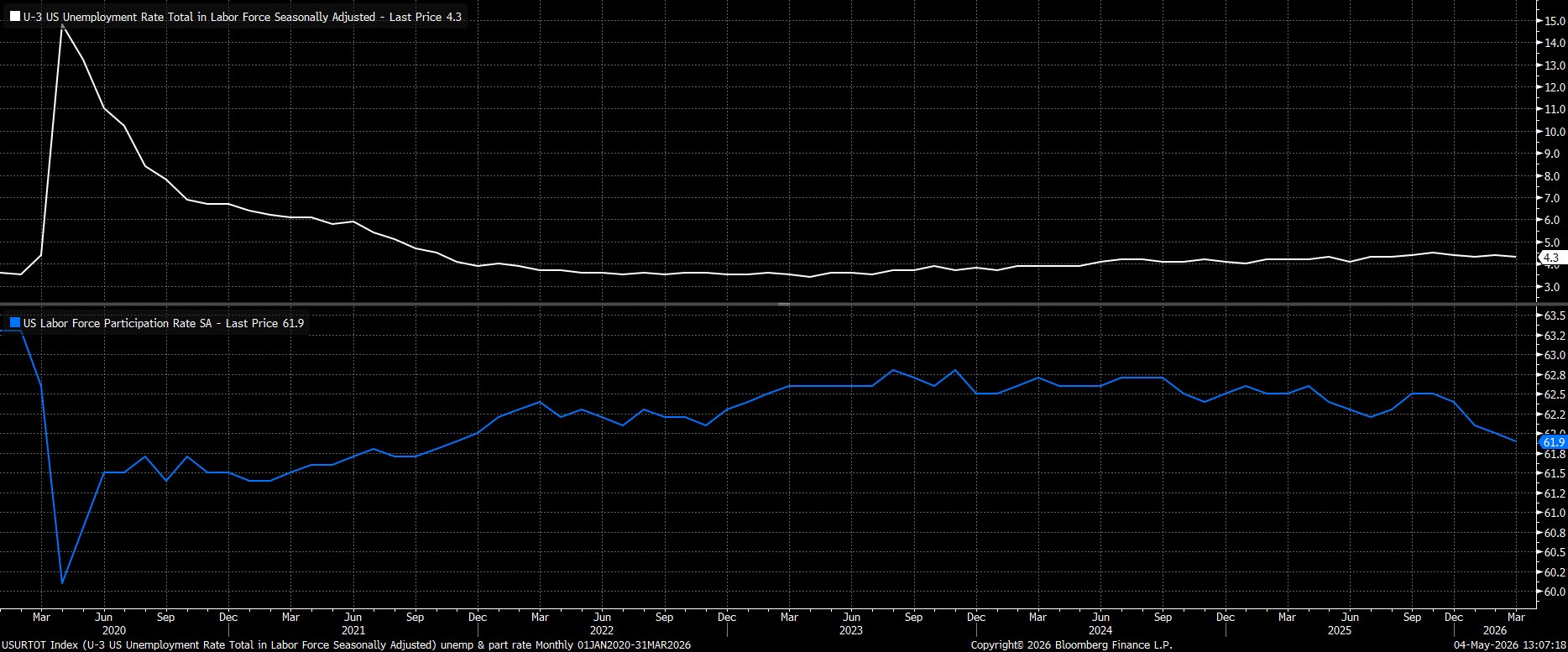

Household Survey Likely Little Changed

Turning to the household survey, headline unemployment is set to have remained at 4.3% in April. However, on an unrounded basis, unemployment actually printed 4.256% last time out, thus providing a relatively low bar for the headline figure to round down to 4.2% in the April report.

As for labour force participation, consensus sees a modest 0.1pp rebound from the cycle low seen in March, to 62.0% this time around.

Few Fed Implications

Taking a step back, the April jobs report seems unlikely to materially alter the FOMC policy outlook. For now, amid uncertainty over both the magnitude, and the duration of the ongoing energy price shock, as well as whether any second-round inflationary effects may emerge, the FOMC are set to retain their ‘wait and see’ approach, standing pat on rates for the time being.

That said, assuming that the inflationary impact of current geopolitical events does indeed prove to be limited, as is likely, there remains a path to delivering one or two rate cuts later in the year, under the stewardship of Chair nominee Warsh. Those cuts could come as a result of the continued ‘no hire, no fire’ labour dynamic prompting a desire to provide a degree of policy accommodation; pre-emptive easing amid belief in an AI-induced productivity boom; or, a need for easing as a result of Warsh being successful in shrinking, and tidying up, the Fed’s balance sheet.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients. Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.