- English

- عربي

A traders week ahead - US CPI and ECB meeting the core events to navigate

This had the effect of pushing down the USD 0.4%, with larger more pronounced moves in the higher beta commodity currencies, with the AUD, NZD, SEK, and NOK finding good buyers. The CAD lagging given Canadian payrolls fell 68k, which had a few questioning the hawkish pricing in the Canadian rates market.

The US headline number of 559k jobs was a solid number, especially when we put in the context of an unemployment rate that fell 30bp (to 5.8%) and hourly earnings rising 0.5% mom. However, it was shy of both the consensus of 675k and where the market was positioned, which was closer to 800k. Progress has definitely been made and the wage data is certainly getting focus as that is highly unlikely to be transitory. However, the US economy is still 7.6m jobs shy of pre-COVID levels and if anything, it possibly reduces the risk that the Fed will refrain from talking about tapering its asset purchase program with any great emphasis at the 17 June FOMC meeting.

The move lower in US Treasury yields, especially with US real yields down 7bp naturally put a strong bid in Tech and Gold, with the yellow metal continuing to hold the March uptrend.

Gold daily

(Source: Tradingview)

US CPI the big event risk for traders this week

It'll be a big week for Gold traders, as it will be for USD traders, with US CPI due Thursday (22:30 AEST), with the street looking for 4.6% headline inflation and 3.4% on the core measure. A 40bp lift in headline inflation (month-on-month) in May is expected and should this prove accurate would be a material life in prices. Importantly, the realised or actual inflation print could impact inflation expectations (or ‘Breakeven’ rates) which will impact real rates, which for fundamental traders are the centre of the universe when it comes to the USD, gold and the NAS100.

A hot CPI print should result in rising bond yields, which will turn the USD around and weigh on Gold and tech. A poor number will have the opposite effect, so it will likely be the event to watch this week. That said, Thursday’s ECB meeting (21:45 AEST) will give the US CPI read a run for being key event risk of the week, with Tuesday’s German ZEW survey also in focus - the fact that German bund yields have fallen from -8bp to -21bp suggests the market is positioned for dovish language to play out, and a belief that the bank will refrain from talking about reducing their own asset purchases program (the PEPP) from its current rate of E80b p/m.

Christine Lagarde will hit the stage shortly after the ECB statement for her press conference, so we hope that we are left with a clearer understanding of the likely path of action in the months ahead.

Any hints that the ECB is falling further behind Fed policy, especially when married with a hot US CPI number could suggest EURUSD is a higher conviction short. That said, the playbook this week is diverse and hard to call and with the market going into the ECB meet expecting a dovish narrative, being short EUR on future policy divergence is tough.

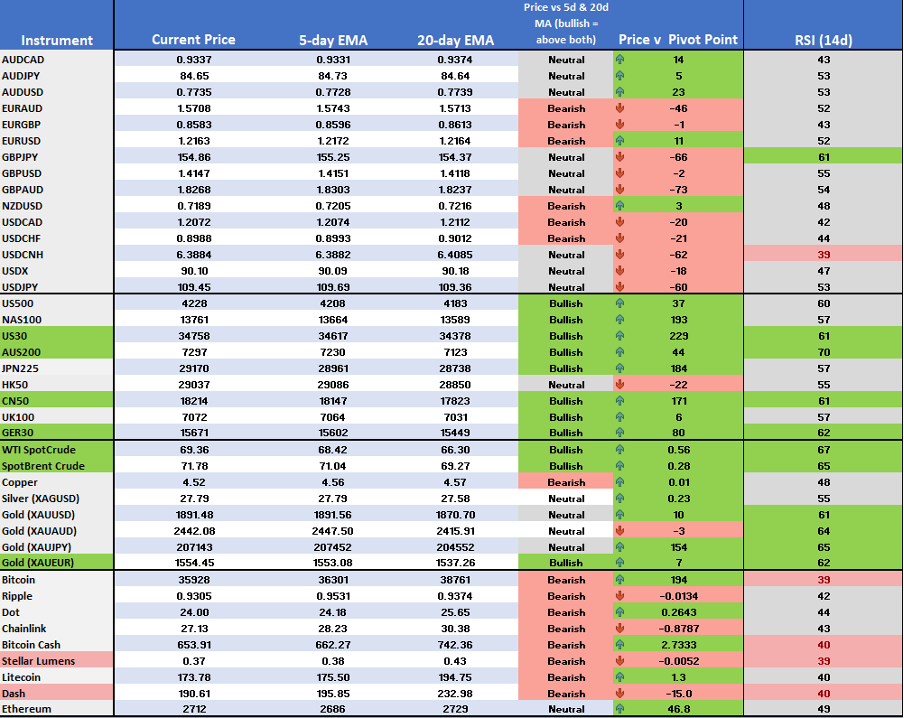

EURAUD could be one to watch for the FX heads this week given the sizeable reversal lower on Friday and I’ll be watching for follow-through as we re-test the breakout highs. My momo model has yet to truly react and offer a short bias, as I like the RSI to be below 40 to show the bear move, but price is below the pivot point and 5 and 20-day EMA.

The EUR catalysts aside, in Australia we see the NAB business and Westpac consumer confidence surveys and RBA member Christopher Kent will be speaking. I don’t see these being a volatility event for the AUD and will likely only modestly plays into the RBA’s thinking as of what to do at its July RBA meeting – a true blockbuster in the making.

The AUD will be largely dictated to by market semantics and bulk/industrial metal prices, but perhaps the bigger driver of China proxies (AUD & NZD) and commodities will be the moves in USDCNH. We’re at levels that have tested the tolerance of the Chinese authorities, so if the cross heads higher and can hold 6.4026 then the USD love may spread through other USD pairs. Should USDCNH fall it may support AUDUSD. Looking at the options market and we can see traders are positioned for USDCNH upside with out-of-the-money calls trading at a higher vol premium to puts. One for the radar.

Our weekend crypto markets get a good run

Weekend Crypto has also been well traded by clients, with some good movement playing out – the Miami Crypto conference certainly got the headlines, perhaps for the wrong reasons, with traders also pushing prices around on news Weibo was suspending certain influential accounts and Goldman saying a CIO roundtable saw Bitcoin as the least desired growth asset. Buyers have supported again, and my momo model is fairly neutral on the coins we offer ex-Dash.

I have my eyes on Ethereum which is consolidating in a triangle pattern. The bulls will want a break of 2896 and this could be back above 3000 in a short space of time.

Ready to trade?

It's quick and easy to get started. Apply in minutes with our simple application process.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients. Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.