- English

- 中文版

US equity trader thoughts - could options expiry prove to be a hidden catalyst?

Consider the average drawdown from its 52-week high in the US500 is 25%, so we can see the index move masks some of the pain felt on a single stock basis.

Clearly, the NAS100 is already in a technical bear market and those who hold high growth stocks and failed to protect against drawdown would certainly attest to feeling this dark sentiment.

With a focus on the US500, the set-up on the higher timeframe is of clear interest.

On the daily timeframe, the move to 3856 while just shy of the 20% drawdown has set the index up for a potential double bottom (DB), so if the bulls can pull a rabbit out of a hat.

(Source: TradingView - Past performance is not indicative of future performance.)

1) A close above the DB neckline at 4097 would target 4340, which is also the 61.8% retracement of the recent leg lower from 30 March. The move needs work but we scan for the bullish triggers.

2) Somewhat more concerning is that we see price currently under the head and shoulders neckline at 4013 – where a weekly close below the neckline would in theory target 3400, just below the 200-week MA at 3480. We saw the bulls defend this level last week, and while we often see many failed H&S patterns, this may certainly come on many traders’ radars, especially with the Fed seeing a lower equity market as a positive and one of the many avenues to create a negative wealth effect.

So, some big levels for the bulls to go after – the session ahead could be telling.

Could options expiry be a short-term bullish catalyst?

One key consideration that has been a major focal point is the idea that the move lower in US equity indices has been due to different types of flow activity, exacerbating the moves lower in NAS100, US30 and US500.

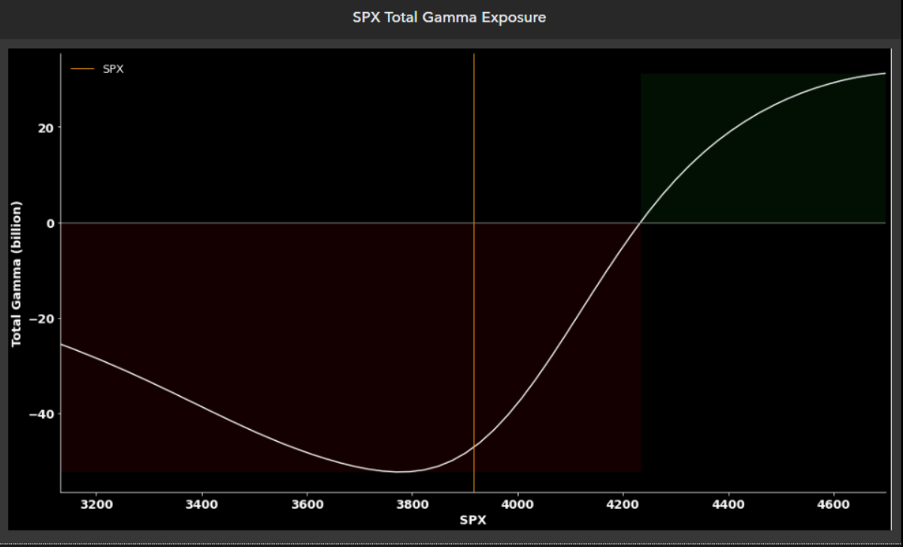

One factor is the way market makers/dealers hedge options exposures – the market has been big buyers of S&P 500 and NAS 100 puts to protect/catalysis on index drawdown – as the respective indices have moved lower and through the fixed strikes of the options dealers/market makers who have sold the options have to dynamically hedge their ‘deltas’ – they are not interested in taking a view on direction, they just short S&P 500 futures to balance out and bring their delta back to zero.

(Source: Pepperstone - Past performance is not indicative of future performance.)

As it stands, I can see dealers running a massive short gamma position – this means the market can be incredibly volatile and the hedging needs by dealers significant. With options expiry (OPEX) due today, we know that a large chunk of this gamma expires – I won’t explain ‘gamma’ and ‘delta’ (there's some amazing intel on options Greeks on YouTube) but for index CFD traders this may mean that dealers will be looking at reducing their inventory of delta hedges (i.e short S&P 500 and NAS100 futures) on Monday, and therefore potentially looking to buy these back.

Could this be a source of inspiration for equity bulls?

Perhaps – so consider after the major equity drawdown in December 2018 and March 2020, the lows and the stage for a subsequent V-shaped recovery came the day after options expiry. Granted both of these occasions came at quarterly expiry which is more significant and that doesn’t come until 17 June. However, in a world where sentiment is shot to pieces and liquidity is so poor, it wouldn’t take much to cause a positive ripple through markets, and as we know the best thing is to always be aware of the triggers and have an open mind.

The technicals are there for all to see and I have levels that can be respected, but the question today is post OPEX could we see dealer's part buy back delta hedges, subsequently proving to be a bullish catalyst, at least for a short-term move?

Related articles

Ready to trade?

It's quick and easy to get started. Apply in minutes with our simple application process.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients. Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.