- English

- 中文版

The fundamental catalysts once again have us questioning the broad moves, but as we know this is a market where we think less and go with the flow.

Like many, I had considered the elevated risk that US fiscal talks could promote greater uncertainty and market volatility should we go to the wire, which was looking like the case given talk from Nancy Pelosi and Senator Perdue yesterday. However, Senate Majority Leader McConnell has given us new hope telling CNN that the Senate will be in session next week – the plan is to cobble a deal together by Friday and have it voted through Congress next week. Who knows, this may well still prove to be a volatility play, but should it pass then the devil is in the detail and the prospect of another economic sugar rush, with $1200 stimulus checks (+$500 per child) for household, clearly inspiring.

US data flags downside risk to US NFPs

On the data side, there was limited fall-out to ADP payrolls which showed 167,000 jobs were created in July – well short of the 1.2m eyed by the market. There have been a few revisions (from economists) to their non-farm payrolls call (Friday 22:30 AEST), although the consensus remains at 1.5m jobs, and I’d argue there is clear downside risk to this consensus estimate. Whether payrolls prove to be a volatility event is debatable – it should be, although obviously, that depends on the outcome. The market is seemingly more concerned about higher frequency data (restaurant bookings, flight activity, initial jobless/continued claims, credit card spending and traffic congestion statistics) and if this stagnates will there be a sustained impact in economics.

More encouragingly we saw the ISM services print in at 58.1, which on the diffusion index portrayed good growth from June and a decent beat to expectations. The new orders sub-component smashed expectations at 67.7, however, the employment sub-component printed 42.1, below expectations – this means employment in the services sector declined at a faster pace on the month – another reason to believe there is downside risk to Friday’s payrolls.

By way of market moves, there is a solid reflections theme through markets. In equities, we’ve seen small caps easily outpace larger caps (the Russell 2000 closed +1.9% vs +0.6% in the S&P500). We’ve seen industrial, material and financials sectors working well, and cyclical stocks have easily outpaced defensive sectors. Commodities are bid, with gold up 90bp to $2038, while silver has gained 3.7%. WTI crude sits up 1.1% and eyeing a break of the 200-day MA, while copper has gained 71bp.

Reflation the theme of the day

In the bond market, we see 5-year US breakevens (average inflation expectations over the coming 5-years) +6bp – this is where we can the reflation in its truest form, with the lift in yield higher than that of nominal Treasury yields and subsequently ‘real’ yields push further lower – we all know the result of lower real US Treasury yields – gold/silver/Bitcoin go bid, the USD attracts sellers, small caps outperform large caps and its rinse wash and repeat.

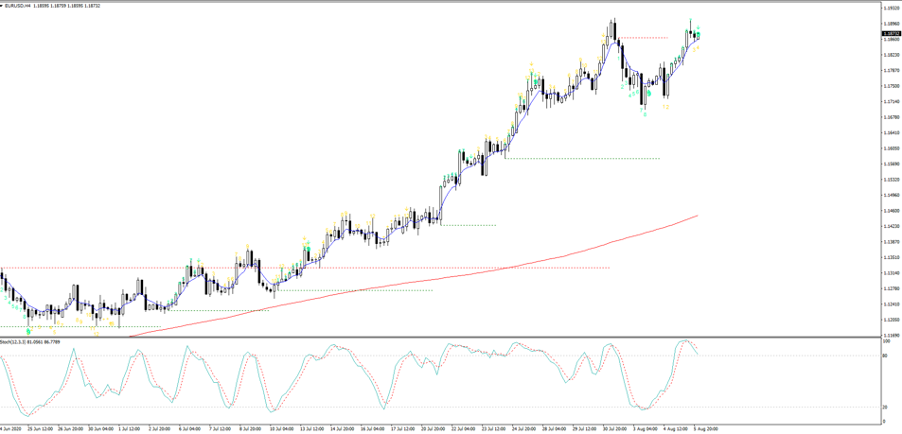

Digging deeper in FX moves, and the USD continues to attract solid client interest, with EURUSD at the heart of that flow. The daily of EURUSD shows solid supply into 1.19 where we see price failing at last week’s high - The mirror opposite can see seen in USDCHF. I see the risk of consolidation at these levels but given the price action and flow it feels like there are more upside risk than downside. That said, my preference is longs in EURJPY and if I was going to play the USD from the short side then short USDNOK looks good and is trading at the weakest levels since January.

All eyes on GBP exposures as we head into the BoE meeting (16:00 AEST). The bank won’t cut, but traders are expecting a slight dovish twist which opens the door for rates to be taken from 0.1% to zero by November. Any potential cut (in November) would presumably be married with £50 to 100b of additional QE (bond purchases) and the language may shift to show an open mind to negative interest rates – a fate currently being priced by swaps markets. Market positioning is fairly neutral, with both leveraged and real money accounts running a small net short in FX futures. In terms of volatility, it’s still quite early in the session but the market expects a move of 82p (higher or lower), which considering skew puts a range of 1.3202 to 1.3056 in play on the day – one for the mean reversion traders. The outlier range is 1.3265 to 1.3000.

Related articles

Don’t miss out.

The Great Debate. 11 July 2020, 20.30 - 01:00 AEST.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients. Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.