CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 72.2% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

- English

- Italiano

- Español

- Français

The smooth passage and passing of stimulus therefore plays into the market's risk premium and a ‘strong’ government, that being where one party controls the White House, House and Senate, would obviously help facilitate that.

Markets would see a ‘strong’ government as a positive for market sentiment, rejoicing on the increased potential for deficit spending. The idea being this would lead to increased inflation expectations and ever deeper negative ‘real’ (inflation-adjusted) Treasury yields that would result in a weaker USD, gold appreciation and broadly higher equities.

To get a ‘strong’ government according to my election probability matrix, the most likely path is we see the ‘Blue Wave’ scenario play out. The notion of a ‘Red Redux’ can't be ruled out either. However, it would require the REP’s to get the House, and for that, they would need to win 27 of the 31 ‘toss-up’ seats, which seems unlikely.

I appreciate many will disagree with my anticipated set of outcomes and many feel that a DEM clean sweep would cause a risk-off tone to markets given their focus on higher tax, energy, regulation and an end of shareholder capitalism. However, I think simplistically the DEM’s are more likely to move closer to a loose MMT (Modern Monetary Theory) model – increasing the deficit and leaning on the Fed to indirectly monetise government debt. The fact we’d likely see Fed governor Lael Brainard appointed as the US Treasury Secretary would also be a huge development.

Judging by my aggregated matrix of various betting markets, average polls and political forecasts, the DEM’s have a reasonable chance of the sweep, although the Senate battle looks really tight. Granted, most, when looking at these variables will immediately say “look at 2016” and how wildly inaccurate these metrics proved to be for traders to price risk. However, to dismiss them seems incorrect and statisticians would have recalibrated and reworked their models and will stress the importance of using a margin of error.

(2020 US election probability matrix – consider the data was napped straight after the debate)

A relief rally to emerge, simply on an accepted outcome?

Strong government aside, after watching the first Presidential debate it’s clear that just getting an outcome that is accepted by the losing party would be enough to avoid a meltdown of markets and a strong risk-off tone. Perhaps, at least in the period when the actual outcome is truly known and all the votes are in, any outcome that avoids a contested election and a probable move to take the decision to the Supreme Court should see a relief rally.

Trump’s comments during the section on “election integrity” that the Supreme Court could be a deciding factor seems key and clearly raise the prospect of contested. As was the comment that "Proud Boys, stand back and stand by”, which seemingly resonated in markets and traders are concerned that tensions spill over into the streets and a test of the social fabric of the US.

S&P 500 options term structure

(Source: Bloomberg)

To back up this view we can either look at the initial negative reaction in S&P 500 futures to these comments, or we can look at the options market. Here we see the S&P 500 implied volatility (vol) term structure (above), which maps out the level of implied volatility for future S&P 500 options expiries (white - puts, calls - red), but it’s the put vol that interests.

As one would expect traders have been hedging risk by paying up for S&P 500 put optionality that expires on the election day (green circle). But then implied volatility, or expected downside movement in the S&P 500, becomes even greater and more expensive right through to the peak in January.

One could argue that we can take this as a sign that traders have hedged their equity risk for the scenario where either candidate fails to accept the outcome and are expecting a cage fight and some ugly scenes that infiltrate the market's psyche.

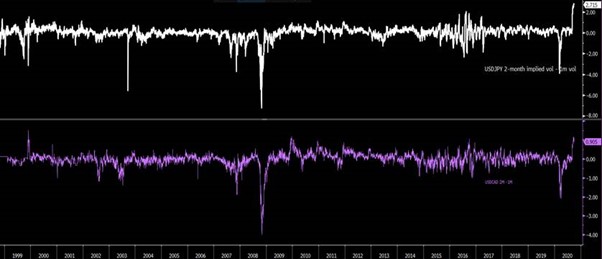

Moving into FX options volatility. If I look at USDJPY 1-month implied vol it sits at 5.97%, which is in no way elevated, but then this expiry doesn’t cover the actual election. If we look forward and at the difference between 2-month and 1-month implied volatility in USDJPY (white), it sits at an all-time high, while the spread in USDCAD (purple) is the highest since 2008. We see a similar dynamic in bond market volatility.

Again, while everyone is looking at the playbook in markets and what it means as to who gets the White House and the make-up of Congress, perhaps the question we should really be asking is "whether we get an actual outcome or whether it is contested". In the near-term, we can see that funds are seemingly hedged through optionality, but the risk of contested could be enough to leave the risk buyers out of the markets. Equity markets could fall just simply on order book dynamics (lack of buyers), with risk FX also facing downside pressure. But, the message from the options market is clear and suggests that perhaps the outcome doesn’t really matter as long as we avoid a contested election. Ready to take a position?

Related articles

Ready to trade?

It's quick and easy to get started. Apply in minutes with our simple application process.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients. Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.