- English (UK)

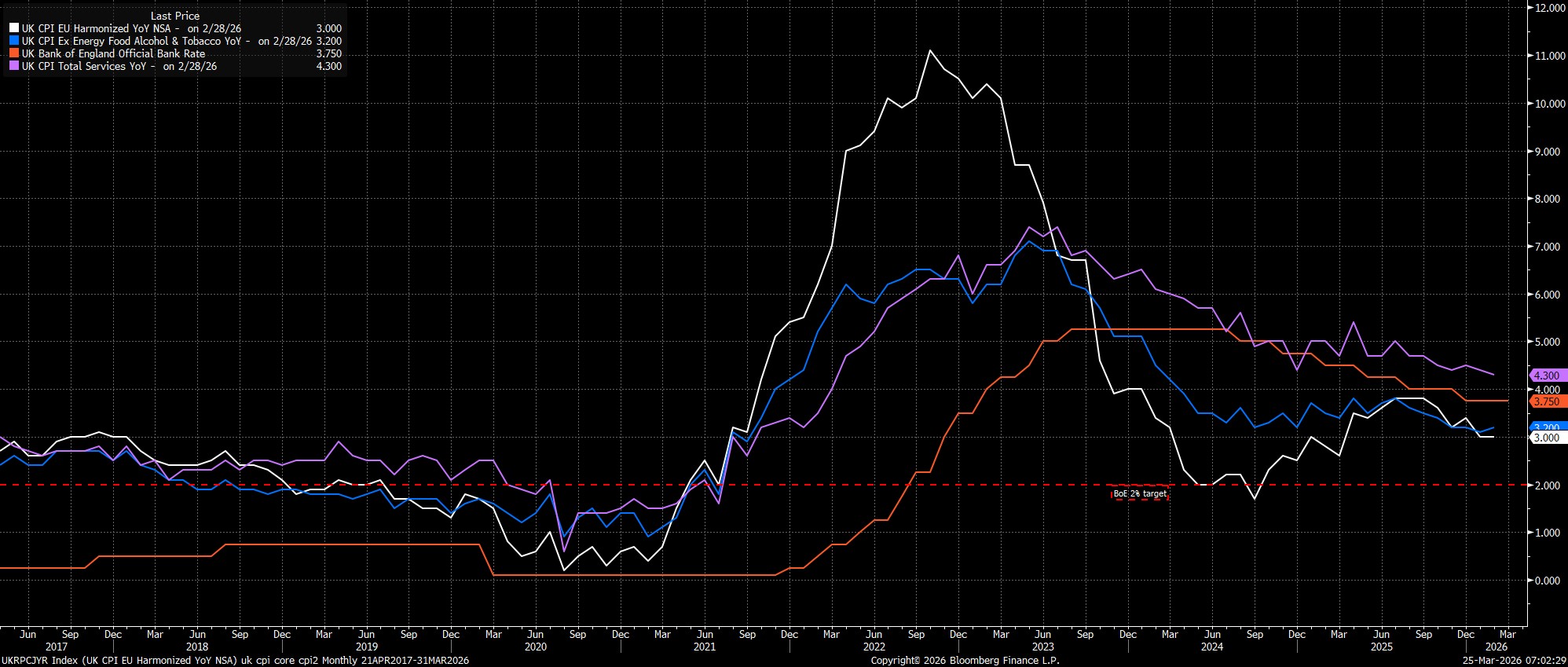

Headline CPI rose 3.0% YoY last month, unchanged from the rate seen in January, and bang in line with the BoE's expectation. Meanwhile, measures of underlying price pressures printed a touch hotter than expected, with core CPI rising 3.2% YoY, and services prices rising 4.3% YoY, the latter being 0.2pp above the Bank's expectations, though still rising at the slowest pace since March 2022.

All that said, at this stage, the data is clearly very stale indeed. Since the February inflation figures were collected, as we are all well aware, conflict has broken out in the Middle East, sparking a sharp rise in energy prices, with Brent crude futures over 40% higher, and front UK nat gas futures almost 75% higher, since the end of last month. Clearly, these sharp increases in energy prices will feed-through to higher headline inflation in the months ahead, with the Bank of England presently expecting CPI at 3.5% YoY in March, though the duration of this higher inflation, and the magnitude of the spike in CPI, will both hinge, almost entirely, on the duration of the conflict, and the time taken for energy flows through the Strait of Hormuz to normalise once more.

With that in mind, today's data shan't matter too much, if at all, in terms of the near-term BoE policy outlook. Still, the MPC delivered a surprisingly hawkish hold at the March meeting, not only voting unanimously in favour of the policy action for the first time in almost five years, but also flagging that policymakers are 'alert to the increased risk...of second-round effects', while being prepared to 'act as necessary' to achieve 2% inflation over the medium-term.

The chances of those second-round effects materialising, however, seem relatively slim to me. Inflation expectations are well-anchored, while a significant margin of labour market slack is present, minimising the potential for a 'wage-price spiral' to take place. Similarly, broader economic momentum remains anaemic at best, leading to minimal corporate pricing power, and further reducing the risk of price pressures proving embedded. Still, scarred from the experience of the post-covid inflation surge, the MPC seem to be fighting the last war and pre-occupying themselves by fretting over a relatively low-probability outcome.

Markets, however, have taken the Bank's hawkish message to heart, with swaps discounting around 74bp of tightening by year-end, and around a 3-in-4 chance of a 25bp hike as soon as next month, as of yesterday's close. With Bank Rate already in restrictive territory, my base case is considerably more dovish than that, seeing the MPC as most likely being on hold for the remainder of the year, providing that second-round effects don't emerge.

Even if they were to emerge, which to reiterate I see as a slim probability, the bar for delivering a rate hike is likely a lot higher than the market envisages it to be, especially with Bank Rate already around 75bp above neutral. If a hike, or more, were to be delivered, this would likely go down as a significant policy mistake, with the Bank tightening policy into a significant demand shock, in turn exacerbating the subsequent economic slowdown, likely meaning that such tightening, and more, would probably then need to be unwound in very short order indeed.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients. Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.