- English

- 简体中文

- 繁体中文

- ไทย

- Tiếng Việt

- Español

- Português

- لغة عربية

- Монгол хэл

Standing Pat On Policy

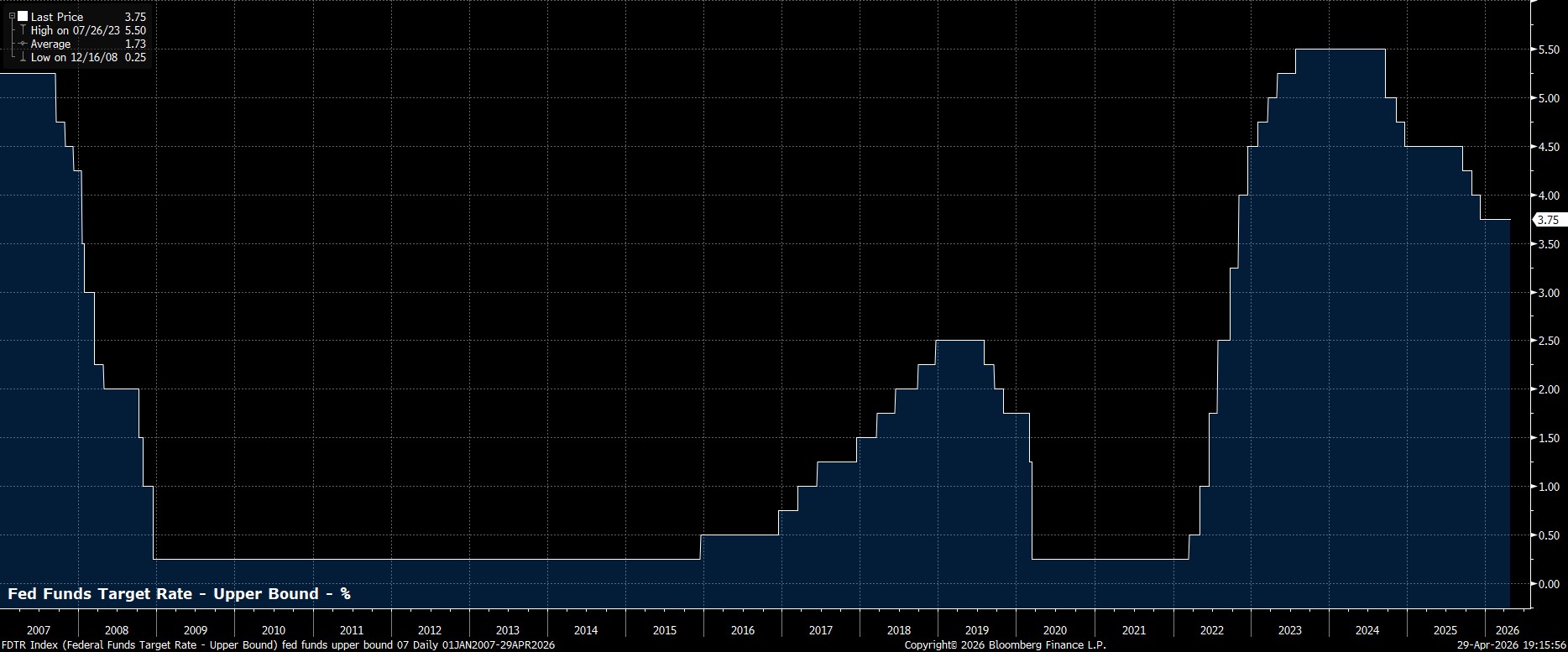

As expected, and as had been fully discounted by money markets in advance of the decision, the FOMC maintained the target range for the fed funds rate at 3.50% - 3.75% at the conclusion of the March meeting.

Such a decision marks the third straight confab at which rates have been held steady, and extends a ‘pause’ in the easing cycle which began at the start of the year, with policymakers continuing to adopt a ‘wait and see’ approach amid the highly uncertain economic outlook, as conflict in the Middle East continues, and upward pressure on energy prices persists.

Divisions Persist

While the rate decision was bang in line with expectations, it once again did not come by virtue of a unanimous vote, with the Committee again divided as to the appropriate course of policy action.

This, though, was not especially surprising, and in any case the dissent in terms of rates was limited once again to the uber-dovish Governor Miran, who is due to depart the Board imminently, being replaced by Chair nominee Warsh. Of more interest, was the three hawkish dissenters – Hammack, Kashkari, and Logan – who, while voting in favour of standing pat on policy, preferred not to include an implicit easing bias in the accompanying policy statement. Still, grandstanding from regional presidents isn’t really anything new, with those three potentially seeking to send a message to incoming Chair Warsh, more than anything else.

Statement Little Changed

Turning to the policy statement, there was little by way of significant changes made compared to the prior iteration.

As such, unemployment was again described as being ‘little changed’, while overall economic activity continues to expand at a ‘solid pace’. Inflation, meanwhile, is now simply described as ‘elevated’, ditching the ‘somewhat’ prefix that was previously present, though the statement clearly tied this uptick in inflation to the recent surge in global energy prices. Of course, that surge stems from geopolitical events in the Middle East, the impacts of which are ‘contributing to a high level of uncertainty’ regarding the outlook, mirroring similar language used last time out.

.png)

Powell’s Final Press Conference

Reflecting on this, at what is almost certain to be his final post-meeting press conference, Chair Powell stuck largely to his recent script. Added to which, markets are, understandably, at this stage, considerably less sensitive to any policy guidance that Powell may provide, considering that Kevin Warsh is set to replace him in the ‘hot seat’ from mid-May.

Of most interest, were Powell’s comments regarding his future, noting that he will remain as a Governor for the time being, albeit while keeping a ‘low profile’ during his remaining tenure on the Fed Board, in light of the continued attacks on the Fed’s independence, and given that the DoJ’s investigation is not yet over with ‘finality’.

Zooming out, many have criticised Powell over the last eight years, almost always doing so with the benefit of hindsight, and almost never while proposing an alternative policy path.

My view is that, all told, Powell has done a damn good job – preventing the repo market seizing up; throwing everything in the toolbox at the economy to support it during the pandemic; taming runaway inflation and engineering a soft landing; all while enduring a seemingly endless series of supply shocks, and staving off unprecedented attacks on the Fed’s independence.

Yes, there have been mistakes along the way, most notably the idea of ‘flexible average inflation targeting’, and the ‘autopilot’ QT slip-up in the early days of his tenure, but the course has been corrected on those fronts relatively quickly. All told, it’s a ‘job well done’ for Jay; as the saying goes, the loudest boos always come from the cheapest seats.

Conclusion

Summing up, the April FOMC changes little in the grand scheme of things, as Powell bows out after eight years at the helm. For the time being, policymakers seem likely to stick with their patient approach, watching how the economy evolves, and how the geopolitical backdrop develops, before making any policy adjustments.

Still, policy tightening remains off the table for the time being, with the direction of travel for rates still being lower, despite those hawkish language dissents mentioned above. Assuming that inflation expectations remain well-anchored around the 2% target, the Committee at large are likely to ‘look through’ the temporary ‘hump’ in headline inflation, particularly given not only the fragile balance in which the labour market finds itself, but also the necessity of a lower fed funds rate if Chair nominee Warsh is successful in shrinking, and tidying up, the balance sheet.

Hence, a couple of rate reductions likely remain on the cards in the second half of the year, particularly if the labour backdrop were to weaken further, though the first of those cuts may not come until September, depending on how the geopolitical landscape evolves.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients. Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.