- English

- 简体中文

- 繁体中文

- ไทย

- Tiếng Việt

- Español

- Português

- لغة عربية

- Монгол хэл

It would appear that, after months of prevarication, and verbal jawboning, Japan’s Ministry of Finance (MoF) have finally run out of patience, stepping up to the plate and intervening to prop up the JPY.

The first, apparent, round of intervention came on Thursday, shortly after top currency diplomat Mimura issued a ‘final warning’ to speculators that the hammer could soon be dropped, with those JPY purchases in turn sparking around a 5 big-figure rally in USD/JPY, with similar moves seen in the crosses. A similar jump in the JPY has been seen early in EU trade this morning, though the move is thus far more modest than the gains seen yesterday, even if it does again have the hallmarks of the MoF getting their hands dirty once more.

What is perhaps most interesting about this intervention round, though, is that it seems centred more on defending a particular level, than about tamping down excess market volatility. It had become a bit of a running joke that USDJPY was trading with a 159 handle every day for the last month, with trading ranges having become very tight indeed. Clearly, the 160 figure in spot USDJPY is a key ‘line in the sand’ for the MoF, and perhaps for the US Treasury too, with whom the Japanese have been co-ordinating on FX matters closely during the course of the second Trump Administration.

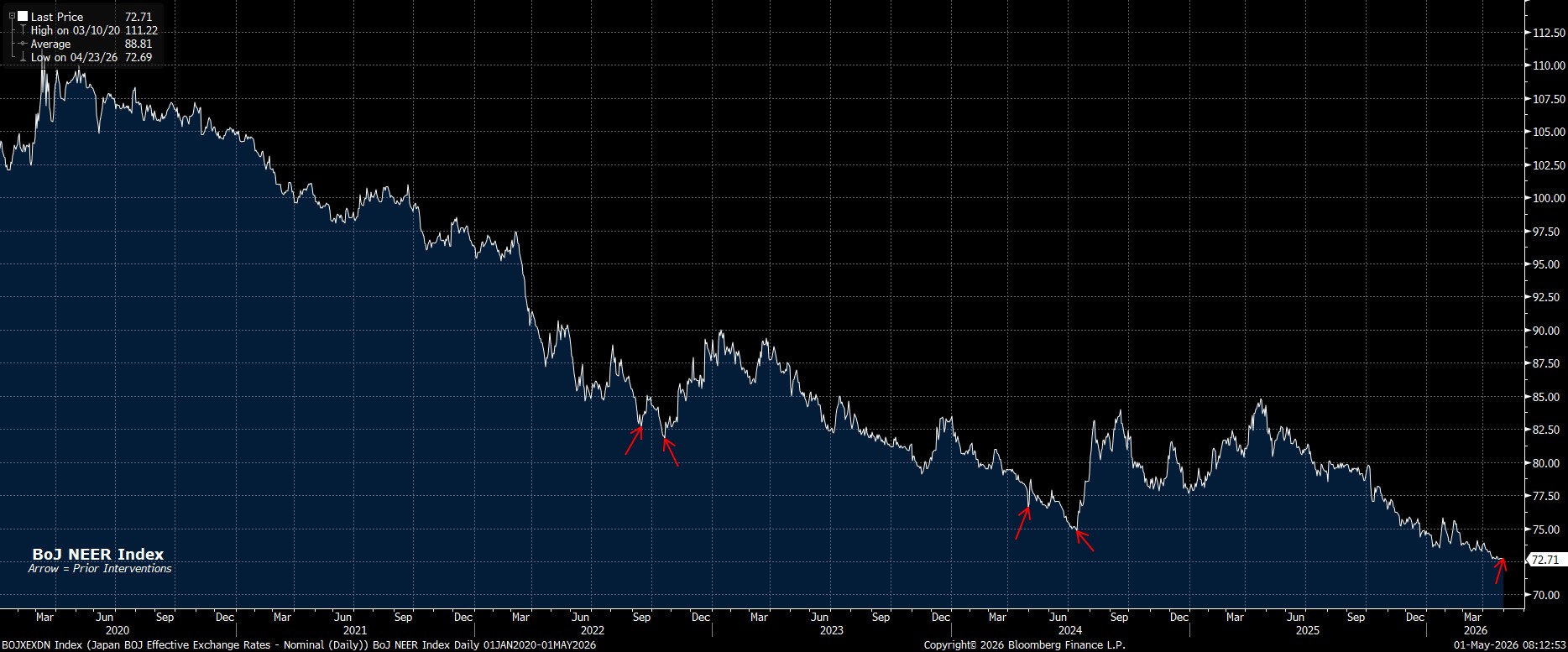

Of course, it is not only spot USDJPY that the MoF will be watching, but the value of the JPY against a basket of peers. If we look at that value, using the BoJ’s JPY NEER index, we see clearly that the JPY is trading at its weakest level in decades. That said, what’s more interesting is that, this time around, the NEER index has weakened just 1.5% over the last 20 days, approx. half the move seen before prior intervention rounds, while we are also only 4% off the 3-month high, again roughly half as far away as we’ve been previously. This, again, suggests that the prior intervention playbook has been torn up, and that Katayama & Co are considerably more pre-occupied with the currency’s level, as opposed to its volatility, then their predecessors.

Zooming out, as is often the case when we see this ‘yentervention’ take place, I would be framing this more as a ‘speed bump’ in the overall trend, as opposed to a move that can change that trend in and of itself.

At risk of stating the obvious, medium-term currency trends are dictated by underlying economic conditions, and those conditions currently don’t augur for sustained JPY strength, given the snail’s pace tightening that the BoJ are embarking on, and the loose fiscal policy that the Takaichi Govt have chosen to run. Unless, and until, that policy mix changes, it’s difficult to believe that sustained JPY appreciation is on the cards.

All that said, what intervention does do is dramatically shift the risk-reward of short JPY positions in the near-term. Few, if any, market participants will want to be short the yen for the time being, with that trade akin to picking up pennies in front of a steamroller. Why would one seek to nick 50 pips or so out of a short JPY trade, while running the risk that the MoF could step in once more, and move the market 5/6/7 big figures offside in the blink of an eye.

That’s likely to keep the market’s tone relatively cautious for the time being, especially with further intervention rounds, as seen this morning, remaining a possibility. Once the dust settles, though, and conditions begin to stabilise, it seems reasonable to expect that the market will look to test the MoF’s mettle once again, and that unless the broader economic backdrop changes dramatically, which seems unlikely at present, further JPY weakness over the medium-term remains likely.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients. Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.