- English

- 简体中文

- 繁体中文

- ไทย

- Tiếng Việt

- Español

- Português

- لغة عربية

- Монгол хэл

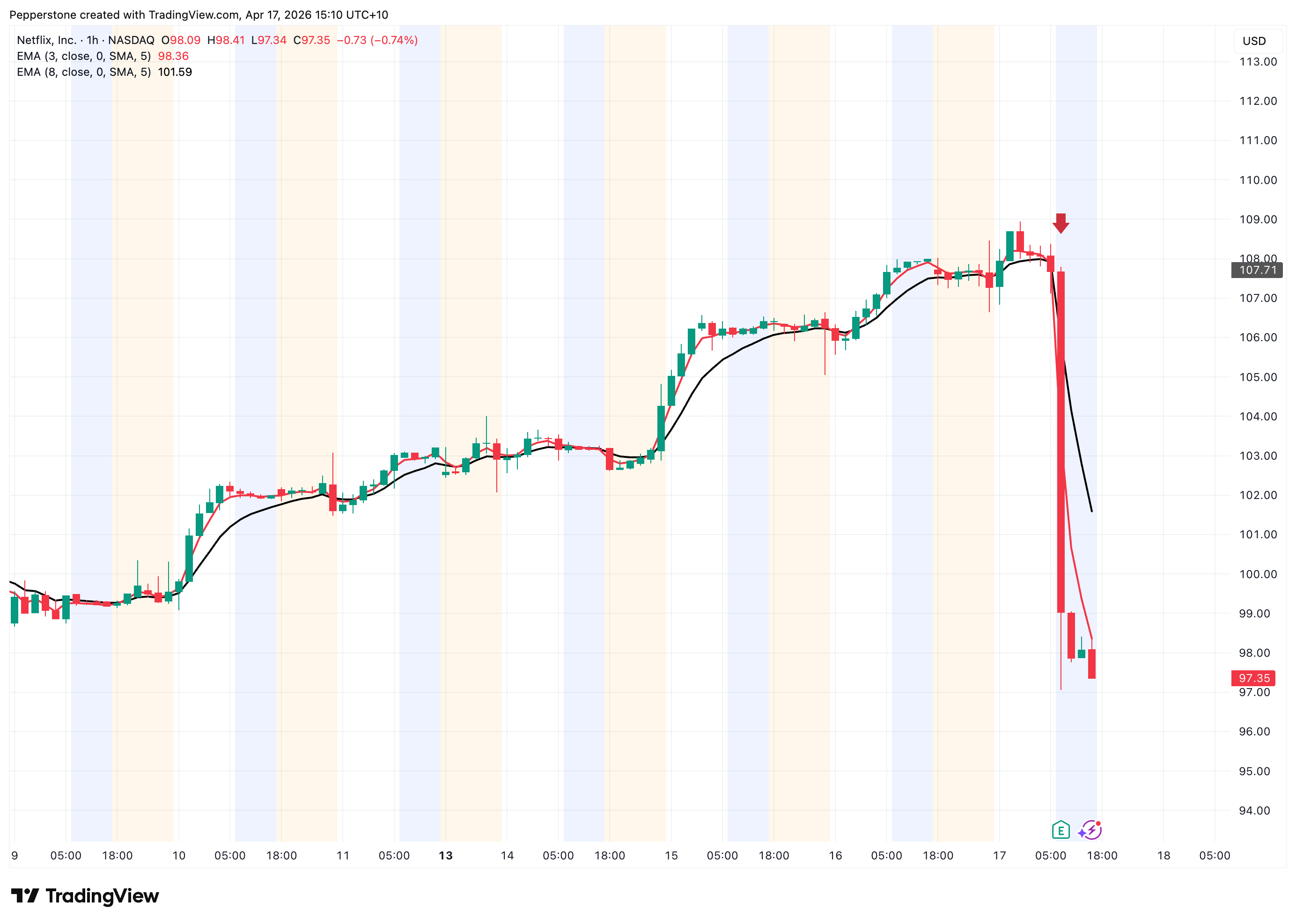

Netflix Q1 26 Earnings Review: Solid Results, Weak Guidance, Valuation Enters Repricing

.jpg?height=93&quality=100)

Netflix (NFLX) reported its Q1 2026 results after the US market close on April 16. Overall performance remained solid: revenue and earnings both came in above market expectations, core operations continued to show steady growth, and both advertising and pricing initiatives kept delivering, while free cash flow also improved notably.

However, the market reaction was notably negative, with the stock falling as much as 10% in after-hours trading.

This seemingly counterintuitive market reaction reflects a shift in valuation logic: the market is no longer rewarding already-delivered growth, but instead reassessing the slope of future growth.

In other words, this was a report where “fundamentals remain strong, but marginal momentum is starting to cool.” At elevated valuations, unless growth expectations are further revised higher, even solid results can trigger a valuation reset.

Revenue and Earnings: Growth Intact, but Quality of Beat Matters

On the headline numbers, Netflix Q1 revenue came in at approximately $12.25 billion, up around 16% year-on-year and slightly above consensus. Earnings were the standout, with EPS coming in at $1.23, significantly above the expected range.

However, this strong figure included a one-off gain of around $2.8 billion, related to compensation from the termination of a deal previously linked to Warner Bros.

As a result, much of the upside surprise was driven by financial items rather than operating acceleration. This also means that, if non-recurring items are excluded, Netflix’s underlying operating profit remains resilient but the degree of beat narrows significantly, without showing the kind of “step-change improvement” that the headline numbers suggested.

Core Business: Resilient Subscription Trends, but Growth Drivers Are Evolving

From a structural perspective, Netflix’s growth framework remains clear, driven by three main factors: steady subscriber expansion, pricing-driven ARPU growth, and continued advertising penetration.

The core subscription business remains highly resilient. Global paid membership continues to grow steadily, with international markets remaining the primary source of expansion.

At the same time, despite recent price increases, churn has remained stable, indicating that content strength and brand loyalty continue to support strong pricing power.

More importantly, advertising momentum continues to build, with management expecting ad revenue to reach around $3 billion in 2026. Against a backdrop of maturing subscription growth, this structural shift is becoming an increasingly important driver of long-term valuation support.

From a strategic perspective, this implies that Netflix is gradually transitioning from a single subscription platform to a dual-engine model: subscriptions providing stable cash flow, and advertising providing incremental growth flexibility.

However, from a financial realization standpoint, the advertising business is still in its early scaling phase, with limited contribution to profits so far. As a result, its valuation support remains more expectation-driven than fundamentally earnings-supported.

Guidance Gap Raises Concerns: No Positive Surprise Is a Negative

The key driver of the post-earnings share price decline was the gap between forward guidance and market expectations.

Netflix guided Q2 revenue and EPS slightly below consensus expectations. At the same time, despite the Q1 beat, the company did not raise its full-year revenue or profit guidance, leaving it unchanged within prior ranges.

Management attributed this mainly to changes in cost timing: content amortization is expected to increase in Q2, creating short-term margin pressure before easing in the second half of the year. While this does not change the full-year trajectory, short-term fluctuations are often amplified in market pricing, particularly when valuations are elevated. Any temporary slowdown can therefore trigger a repricing move.

In addition, news that co-founder Reed Hastings is gradually stepping down from the board has drawn attention to strategic continuity, further contributing to cautious market sentiment.

From Growth Premium to Cash Flow Pricing

Overall, the post-earnings share price reaction does not reflect a deterioration in fundamentals, but rather a subtle shift in the investment narrative. The company is moving from a high-growth platform toward a more mature phase of stable growth supported by cash flow generation, while the valuation still partially reflects a growth-stock framework, leading to episodic profit-taking.

Looking ahead, Netflix’s key variables are likely to focus on three areas.

First, whether subscriber growth is entering a true plateau phase. If North America continues to mature and international growth also moderates, overall expansion will rely more on pricing and mix optimization rather than scale.

Second, the quality of advertising monetization. The key question is not only the scale of ad revenue, but also whether ad load affects user experience and whether advertiser budgets can translate into stable and recurring revenue streams.

Third, the long-term balance between content investment and earnings stability. The structural constraint in streaming remains content cost, and long-term profitability will depend on sustained improvements in content ROI rather than cost-cutting alone.

In the medium to long term, Netflix continues to evolve toward a global entertainment infrastructure platform. However, the investment narrative has clearly shifted from accelerating growth to a reassessment of earnings stability and cash flow quality.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients. Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.