- Français

- English

- Español

- Italiano

As always, it makes sense to be aware of the themes and trends in markets to gain insight into the probability the moves continue. Fed speakers dominate this week, notably speeches from Clarida and Brainard with a clear focus on whether they detail what tools they have to drive up inflation.

We watch to see if the Fed speakers can drive up inflation expectations and drive down ‘real’ Treasury yields. If they can do this then the USD should continue to trend lower and gold and high growth equities will continue to rally. That’s a big ‘if’, but if the Fed is to be successful they need to get the markets to believe they are credible, which could have big implications for assets.

Politics in the US and now Japan (with Abe stepping down) also garner attention. Reports that the UK Treasury will raise the corporate tax rate to 24% (from 19%) may impact on GBP and the UK100. We have central bank meetings in Australia and tier-one economic data in the US.

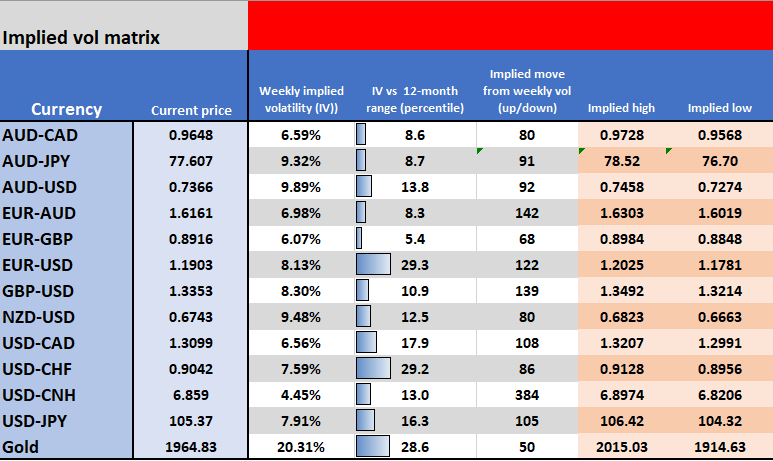

Implied volatility matrix (using option’s pricing from Friday’s close) help us to understand what the market is implying for movement and the expected moves, either higher or lower.

What’s on the risk radar?

* Event risks (as indicated) are potentially an impactful event.

Monday

China – At 11:00 AEST we see August manufacturing and services PMI. The market expects a slight improvement in manufacturing with the diffusion index moving to 51.2 (from 51.1), while services should remain in growth territory at 54.2. The data is unlikely to miss the mark to any great degree, so one suspects it holds a low risk of being a volatility (vol) event.

USDCNH is a key cross this week and while unlikely to be impacted by the data, if USDCNH breaks 6.8457 (Jan low) then it will resonate with USD selling across G10 FX. This could see AUDUSD pushing towards 0.7400. Conversely, should we see shorts covering (in USDCNH) then it should act as a headwind for the USD bears.

Germany – August CPI (22:00 AEST). The market expects inflation at 0% MoM and 0.1% YoY. This is not a risk for EUR exposures in my view, as it would take a sizable miss to move the dial too greatly. EURUSD looks set for another tilt at 1.1950, although momentum oscillators are showing divergence and are printing a series of lower highs. With so many key Fed speakers this week the moves will be dictated by the USD. I’ve been suggesting to watch EURAUD for a move into 1.6150. If this goes then the target is 1.6020/00.

EU – August CPI estimate (19:00 AEST). The market expects this to fall 20bp to 0.2% YoY. Unless we see a huge deviation from expectations, the inflation data isn’t expected to be a vol event for the EUR or GER100. That said, it does aid fuel to the issue if the ECB takes a more dovish turn at the next official meeting on 10 September.

US (event risk). Fed vice-chair Clarida speaks on the Fed’s ‘Monetary policy Framework’ (at 23:00 AEST) and this will be the must-watch event risk of the week. Last week we saw Jay Powell release the Fed’s long-run goals ahead of schedule, welcoming in a new dawn of Average (or flexible) Inflation Targeting (AIT) and running the economy hot.

However, there are still so many questions. Notably, how they plan to drive inflation expectations and subsequently underlying inflation above target. The Fed needs real yields to move deeper negative to have any chance of success. Clarida’s speech could aim to steady the ship and offer new insights ahead of the 18 September FOMC. The US Treasury market and the USD will be central to markets here.

Chart of importance - The Fed’s 5y forward inflation gauge currently sits at 1.60%, showing the market expects 1.6% average inflation 5-10 years from now. Can the Fed push this towards 3%?

(Source: Bloomberg)

Tuesday

Australia – At 11:30 AEST we get Q2 Balance of Payments (consensus $13.0b), with net exports expected to add 1 ppt point to Wednesday’s Q2 GDP print. The surplus is expected to increase to $13b, which will seem healthy for those looking at this relative to GDP. Although, the reality isn’t the case and real imports and exports will both face heavy declines.

RBA policy statement (event risk). At 14:30 AEST we see the market is not expecting any surprises from the Reserve Bank, with a somewhat more concerned tone expected given the restrictions in Melbourne. There will be focus on renewed asset purchases, with the bank increasing their cumulative govt bonds this month by $8b to $59.348b. Its view on the AUD is unlikely to shift at this stage despite the AUD emerging as a key beneficiary of the Fed’s plan to target inflation expectations. Consider that in a world where central banks must stay in step with the Fed, a more neutral tone could reinforce the AUD as a favoured currency right now.

China – Caixin manufacturing and services PMI (11:45 AEST). The consensus is for the diffusion index to come in at 52.5 and 54.0 respectively. Again, unless these miss the mark it’s unlikely to cause too many ripples through markets. I’ll be watching USDCNH for broader USD moves.

Canada – Markit August manufacturing PMI (23:30 AEST). There is no consensus to work off, so it’s unlikely to impact vols too greatly. USDCAD sits at the lowest levels since January but the flow comes from the USD this week and moves in ‘real’ US Treasury yields. Obvious support into the round number 1.3000 with extreme selling capped into 1.2950, where mean reversion traders will be keen to play.

Wednesday

US (event risk). August ISM manufacturing (00:00 AEST). The market expects the diffusion index to come in at 54.5 (from 54.2), showing an improvement in manufacturing growth from July. As always, the market is keen to see the sub-components with new orders and new export orders will be closely watched. So too will be prices paid given inflation is so important for the markets. The employment sub-component will likely remain below 50 but should not guide expectations too intently for Friday’s NFP, given the relatively small contribution manufacturing offers for the US economy.

Australia – Q2 GDP (11:30 AEST). The market expects a 6% decline in QoQ GDP (the economists’ estimates range from -3% to -13%) and a 5.2% contraction YoY. Unlikely to shock too greatly and therefore shouldn’t be a vol event for the AUD.

UK – BoE members Bailey, Bowe, Brazier, Ramsden and Vlieghe speak (23:00 AEST). Obviously watching GBP exposures with GBPUSD breaking out of its 1.3260 to 1.3000 range. The options market could be seeing (with a 68.2% degree of confidence) the upside on the week capped into 1.3476 and an extreme move into 1.3550 (as priced by 10-delta strangle).

(GBPUSD daily)

US – At 22:14 AEST we see the ADP private payrolls, with the consensus set at 950,000 jobs created in August (estimates range from 1.49m to 700k). Depending on the outcome this could cause a few economists to review their NFP estimate (due Friday), but shouldn’t shake markets too greatly.

US (event risk). Fed Governor Lael Brainard speaks on the new Monetary Policy Framework (03:00 AEST). Another major event risk for traders this week, given Brainard is one of, if not, the most respected Fed officials and what she says carries just that bit more weight. Another where US Treasuries, the USD, NAS100 and gold could have a move.

Thursday

US – NY Fed Governor John Williams speaks on COVID-19 (at 00:00 AEST). While the topic is not a market mover, there’ll be a Q&A session afterwards. Cleveland Fed president Loretta Mester discusses the US outlook and Monetary policy at 02:00 AEST. Mary Daly then speaks on an ‘Economic Framework for the Future’ at 08:00 AEST.

US – Weekly initial jobless and continuing claims. The market expects these to come in at 950k and 14m respectively. With payrolls out on Friday, claims will likely get overlooked. Unless of course, there is a large beat or miss that has traders questioning the recovery.

Friday

US – August services ISM (00:00 AEST). The market expects the service sector to grow at a slightly slower pace in August, with consensus at 57.0 (from 58.1 in July). This is a key data point but not one I’m too concerned with holding exposures over.

Australia – July retail sales (11:30 AEST). The market expects a solid 3.3% rise in retail sales. A decent beat is probably good for 10 pips in AUDUSD, so not one I see as a vol event.

US (event risk). Fed member Charles Evans speaks at 02:30 AEST on the ‘Economy and Monetary Policy’. Evans has been a leading campaigner for AIT of late, so his address is certainly timely. A more detailed understanding of the methodology or formula, by which the Fed will tolerate any potential inflation overshoot would be good. On the surface, it feels like the collective would be comfortable with inflation rising as high as 3%.

Canada – August employment report. The market expects 250,000 jobs to be created (economists’ range 375k to 84k), with the unemployment rate due to fall from 10.9% to 10.1%.

US (event risk) - August non-farm payrolls (NFP). The market expects 1.4m jobs to have been created (economists’ estimates range from 2.4m to 500k), with the unemployment rate due to fall to 9.8% (from 10.2%). Average hourly wages are expected to fall to 4.5% YoY. A good jobs report could push USDJPY higher and underpin bullish moves in US equity markets. Poor numbers will likely hit the USD and boost gold, as it reinforces the idea of the market questioning the Fed’s commitment to go after inflation.

Related articles

Ready to trade?

It's quick and easy to get started. Apply in minutes with our online application process.