Summary:

• Constructive start to the week driven by geopolitical easing and USD selling

• Equity markets evolving into a stock picker’s environment with low correlation

• Key earnings from Palantir, AMD, ARM, Snap, Coinbase and CoreWeave

• US non-farm payrolls the major macro catalyst this week

• RBA expected to hike by 25bp, with debate on whether it marks the final move

• Volatility easing, but markets pricing in a high degree of good news

A Constructive Start to May

We turn the page on what was an incredibly lively month of April for traders and investors, and we refocus on the risks and trading environment that will be presented to participants through May.

Proceedings start on a fairly constructive note, with headlines emerging early as interbank FX markets ramp up, with modest USD selling the initial bias. AUDUSD is notably pushing north of 0.7200, all suggestive of a small pop higher in S&P500 and NAS100 futures, which undoes much of the buying fatigue seen in Friday's price action.

Headlines of "very positive" discussions with Iran have hit the wires, headlines we have become quite accustomed to hearing, but they come with signs of progress. Trump will allow select vessels to pass through the Straits of Hormuz today if they have held a neutral bias on the conflict, aiming to frame this as an easing of logistical constraints for vessels that have been stuck in or around the Straits for some time. Trump will no doubt look for a PR angle as well and suggest a humanitarian perspective, but the market will take kindly to such progression. We should see crude futures opening some 2% lower, which would flow through into risk markets, with inflation expectations pulling back modestly and some rate cut expectations building in US rate markets. Asian equities should also benefit and take some tailwinds from this.

A Stock Picker’s Market

The sellers on Friday started to gain more sway, and with the market discounting so much going right, and equity markets already rallying on earnings euphoria, dispersions in performance have become increasingly evident. The environment is far more attuned to a stock picker’s market. We see that with S&P500 one-month realised correlation falling to 6%, one of the lowest levels of the year, and one-month implied correlation falling back to 11%.

With 63% of S&P500 companies having reported quarterly earnings, the scorecard shows that 81% have beaten expectations on earnings per share by an average of 20%. 72% have beaten on the revenue line, with an average beat of 2.1%. The average stock has moved +/-4.6% on earnings day, highlighting the sizeable moves seen on the day of reporting as the market digests earnings and operating conditions, but also within sectors, with large dispersions in trends and performance. A rising tide is not lifting all ships in this environment.

Earnings Flow and Key Technical Levels

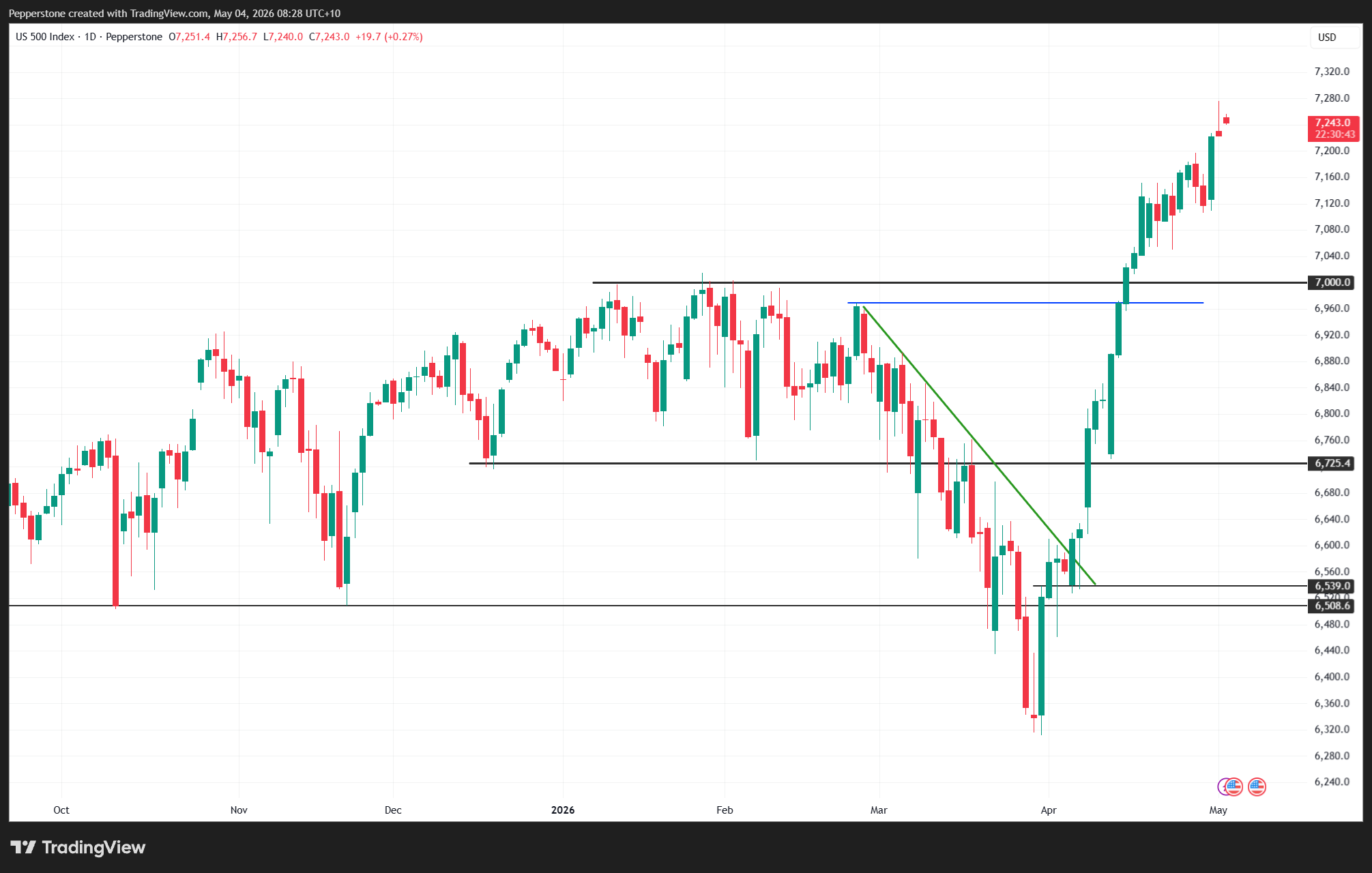

In the coming week, we have a more modest 11% of S&P500 market cap due to report. The generals within the S&P500 have largely reported, with Nvidia still to come on 20 May. This week includes trade favourites such as Palantir, AMD, ARM, Snap, Coinbase, and neoscalers such as CoreWeave. For those set long in risk positions, S&P500 futures ideally need to build and push through 7,250 to make a move towards recent highs of 7,300. Bulls would also like to see the USD index break convincingly through 98, and Brent crude head towards $100.

US Data and Fed Expectations

On the data side in the US, we get the JOLTS report, ISM services, and the key event on Friday with the non-farm payrolls report. The market is looking for moderation in hiring, following the prior strong 178,000 jobs print in March. The median estimate from economists is for 62,000 jobs in April, with private sector payrolls at 75k, and the unemployment rate expected to remain at 4.3%. Forward interest rate swaps markets see the Fed fully on hold over the next 12 months, but a moderation in crude pricing could bring back expectations for rate cuts. By the end of the week, that view on Fed policy and positioning will be shaped not just by crude pricing and inflation markets, but also by labour market data and rhetoric from the many Fed speakers scheduled this week.

RBA Decision and the Path Ahead

The RBA meeting on Tuesday is unlikely to affect global markets and will be confined to Australian assets. Given recent inflation dynamics, a 25 basis point hike this week appears to be a fairly assured outcome, with the market implying a 75% probability. Where there is more debate is what happens next. Interest rate traders are convinced we will see another hike in either June or August, which would take the cash rate above post-COVID levels seen before the rate cutting cycle in February 2025.

There is a growing debate as to whether this week could mark the final hike in the cycle. The Q1 GDP numbers, released on 3 June, will almost certainly mark peak growth in the Australian economy. We are likely to see demand cooling following the 12 May budget, alongside the impact of a higher cost of capital and ongoing cost of living pressures. GDP is then expected to move from 2.6% in Q1 to around 1.5% by year end, with private sector demand and government consumption both slowing. The RBA will be aware of this, and the statement this week will likely adopt a more cautious tone. It is entirely plausible that rates are increased this week, but that this marks the final hike in the cycle, something the market is not yet pricing.

Global Central Banks and FX Dynamics

Elsewhere, we have central bank meetings in Norway and Sweden, although they are unlikely to shift markets significantly. Focus will remain on Japan. While market holidays will reduce liquidity, the yen could still see direction this week after being the strongest performer in G10 FX last week. EURJPY was notably weak, although demand emerged below 184 into 183. Given the holidays in Japan, price action may be driven more by USD flows tied to geopolitical developments, alongside movements in Brent and WTI, and how incoming US data influences front-end Treasury yields and short-term inflation expectations.

Volatility and Market Positioning

Volatility markets have normalised to an extent, with hedges partly reduced and unwound. In crude, the OVX has fallen to 75%, while S&P500 volatility has eased, with the VIX settling around 17%.

European equity indices have underperformed recently, with US exceptionalism becoming an increasingly dominant theme, but earnings ramp up this week with over 20% of the EU Stoxx index reporting. We will need to watch volatility both at the single stock level and across European markets. After a strong April for risk assets, we need to remain open-minded about what May will bring. This week should provide early signals, but with risk assets pricing in a lot of good news, and rightly so, the time for that to be validated may now be here. As always, price will dictate sentiment.

Good luck to all.

此处提供的材料并未按照旨在促进投资研究独立性的法律要求准备,因此被视为市场沟通之用途。虽然在传播投资研究之前不受任何禁止交易的限制,但我们不会在将其提供给我们的客户之前寻求利用任何优势。

Pepperstone 并不表示此处提供的材料是准确、最新或完整的,因此不应依赖于此。该信息,无论是否来自第三方,都不应被视为推荐;或买卖要约;或征求购买或出售任何证券、金融产品或工具的要约;或参与任何特定的交易策略。它没有考虑读者的财务状况或投资目标。我们建议此内容的任何读者寻求自己的建议。未经 Pepperstone 批准,不得复制或重新分发此信息。