Beginning with emerging markets, clients are now able to trade on the following NDF products – USD/BRL, USD/IDR, USD/INR, USD/KRW, USD/CLP, USD/COP and USD/TWD. Covering a range of geographies and a diverse mix of economies, this suite of products brings numerous themes to mind.

The TWD, for example, is likely to spend the medium-term stuck in something of a geopolitical pinball machine, as China-Taiwan relations remain extremely tense, with many seeing a Chinese attack on the island as a distinct possibility, given President Xi’s stated aim that “reunification…must be fulfilled”. On this note, upcoming elections in Taiwan will be closely watched, with the pro-China vote likely to be split among two parties, though even an unprecedented third term in power for the incumbent Democratic Progressives may weaken what is a fragile status quo, pressuring the currency.

_2024-01-05_08-36-21.jpg)

Of course, one must also consider semiconductors when it comes to the Taiwanese economy, with TSMC accounting for around a third of global sales, while also holding a similar weight in the nation’s benchmark stock index, which has more than doubled since 2016.

Other notable Asian currencies to be listed include the INR, where the balance of risks appears to point towards further strength, though continued RBI intervention has kept the currency in a very narrow range for the time being. The KRW is also of interest, with exports remaining the main driver of the currency, though the BoK are likely to begin cutting rates from H2 onwards, timing that is likely to be roughly in line with most DM central banks. On that note, MSCI have yet to classify South Korea as a developed market, noting the need to monitor the implementation of a range of policy reforms that are currently taking place within the country, though eventual inclusion (if it were to occur) is likely to result in significant overseas inflows into the KOSPI, also providing the currency with a helpful boost.

Meanwhile, in South America, Pepperstone clients can now gain exposure to a broader range of LATAM economies, being able to trade the BRL, CLP, and COP.

Disinflation has continued across the region of late, with central banks in both Brazil and Chile having embarked on what are likely to be relatively aggressive easing cycles. While rates in both nations are likely to fall towards the 7% region over the course of the year, the negative impact of such a move on the respective currencies may well prove to be limited, with real rates likely remaining north of 4%, therefore continuing to represent an attractive yield for international investors.

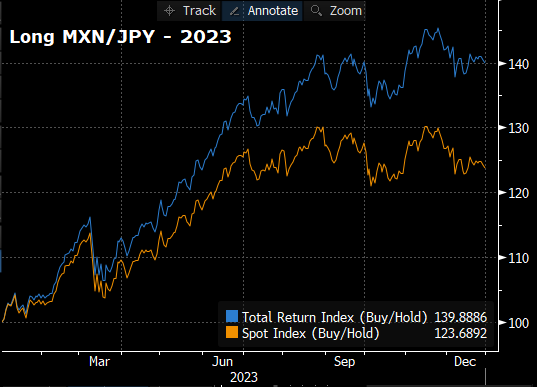

_2024-01-05_08-33-30.jpg)

Sticking with LATAM, it’s worth mentioning the MXN/JPY, which was the standout performer in the FX world last year, where a long position held all year would’ve returned around 20% on a spot basis, and almost 40% on a total return basis when carry is included.

However, this trade’s tide may be starting to turn, as the Banxico appear set to also begin an easing cycle in 2024, with minutes from the final meeting of last year flagging the likelihood of ‘gradual’ cuts being delivered over the next 12 months. Couple this with the likelihood that 2024 is, at long last, the year the BoJ finally exit years of ultra-easy policy and move rates back into negative territory, and a significant chunk of those carry bets placed last year are likely to begin to unwind.

Elsewhere, a handful of other interesting crosses spring to mind among the new listings. For instance, clients are now able to trade the CNH against the EUR, GBP, and the NZD, allowing traders new ways to gain exposure to the world’s second largest economy, where a full recovery from the pandemic-induced downturn remains elusive, despite ever-increasing amounts of government stimulus.

The CHF also stands out, with the SNB having been arguably the most successful G10 central bank in bringing inflation back to target, and having recently softened its language on the currency, removing its bias towards selling the CHF. With CPI now running at 1.4% YoY, and the ECB likely to loosen policy as soon as March, there is an increasing likelihood that the SNB also embark on a relatively rapid easing cycle.

Short CHF/NOK may well prove to be the trade here, with the Norges Bank having surprised in a hawkish direction with a 25bp hike to round out 2023, and indicating that rates will remain at 4.5% for “some time to come”, with headline CPI continuing to hover around the 5% mark.

此处提供的材料并未按照旨在促进投资研究独立性的法律要求准备,因此被视为市场沟通之用途。虽然在传播投资研究之前不受任何禁止交易的限制,但我们不会在将其提供给我们的客户之前寻求利用任何优势。

Pepperstone 并不表示此处提供的材料是准确、最新或完整的,因此不应依赖于此。该信息,无论是否来自第三方,都不应被视为推荐;或买卖要约;或征求购买或出售任何证券、金融产品或工具的要约;或参与任何特定的交易策略。它没有考虑读者的财务状况或投资目标。我们建议此内容的任何读者寻求自己的建议。未经 Pepperstone 批准,不得复制或重新分发此信息。