差價合約(CFD)是複雜的工具,由於槓桿作用,存在快速虧損的高風險。80% 的散戶投資者在與該提供商進行差價合約交易時賬戶虧損。 您應該考慮自己是否了解差價合約的原理,以及是否有承受資金損失的高風險的能力。

.png)

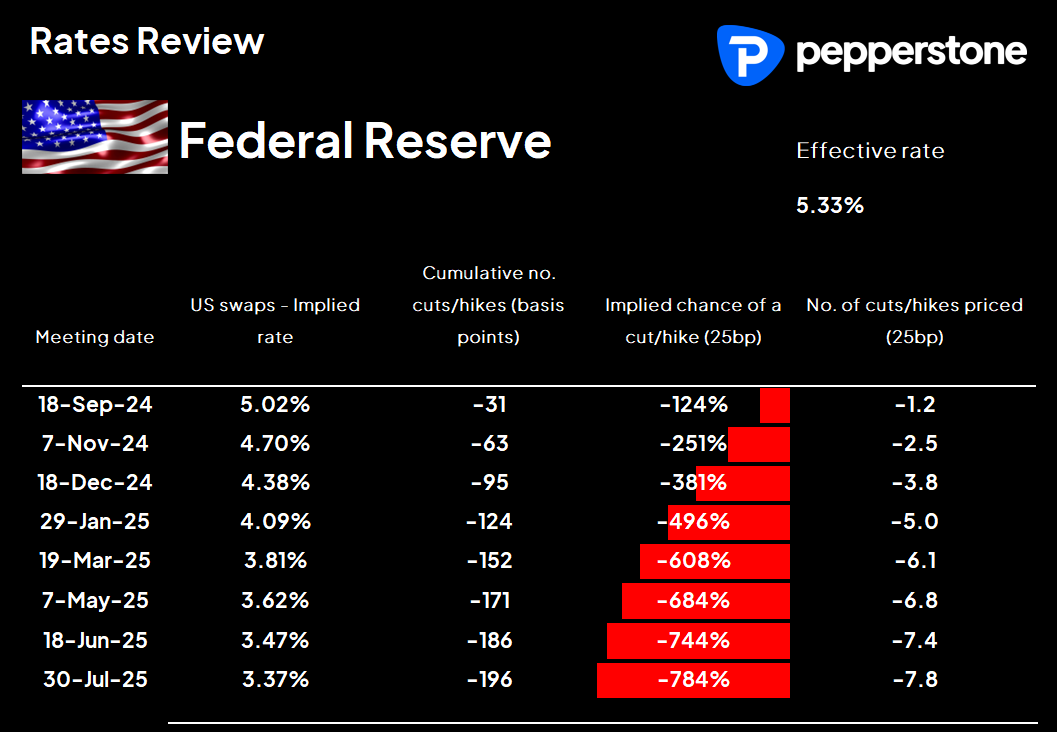

透過市場定價,美國利率互換價格顯示9月FOMC會議預計會降息31個基點(或50個基點降息的機率為25%),並預計到12月將降息95個基點。這是本週市場的第一個導數,利率預期的變化應該引導股市、美元和黃金。

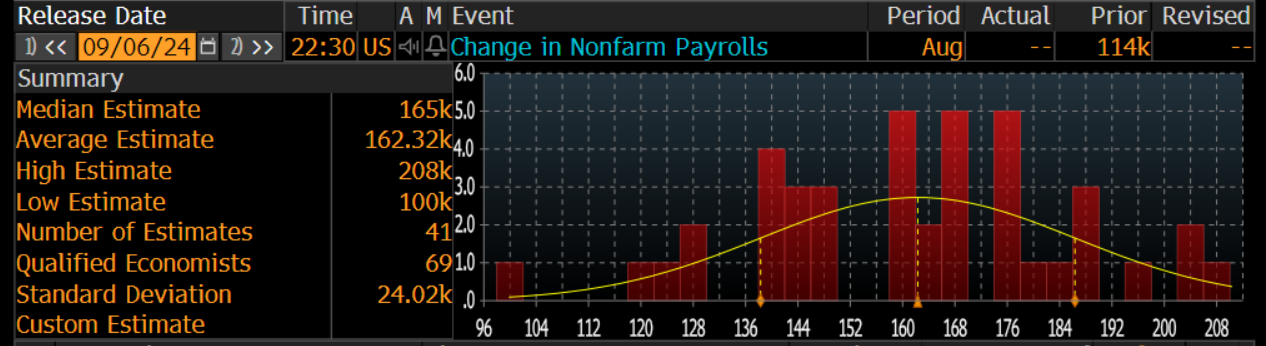

如果非農就業人口報告表現疲弱,例如低於13萬,同時失業率維持不變,我們很可能會看到利率市場更接近於定價50個基點的降息。如果非農就業人口報告的結果強於市場預期,那麼25個基點的降息將成為默認位置。

另一個重要考慮因素是聯邦儲備委員會理事沃勒在非農就業人口報告發布後2.5小時發表講話,展望美國經濟的前景。交易員將更清楚地了解克里斯托弗·沃勒對就業報告的看法,他的觀點與FOMC成員中的任何人一樣重要。

從戰術上看,好消息應該對風險資產有利,更好的數據可能會推高股市和美元,25個基點的降息是美聯儲真正想要的舉措,因此進一步證據表明美國經濟正朝著軟著陸發展,伴隨非緊急降息的背景對風險資產形成了一種理想的環境。

50個基點的降息聽起來對股市是積極的,但我不確定是否會產生這種情況,勞動力市場的不利消息可能會導致股市賣盤增加 - 至少在股市更周期性的領域 - 和美元再度走低。

審查更高時間框架圖表

考慮到上述美國數據流,我們審查每日和每周大圖表,以評估潛在近期方向的概率評估,這可能會影響我們看待風險平衡的方式。

在股指方面,提供最大潛力繼續向上風險的設定出現在S&P500、NAS200、NKY255、DAX30和SPA35 - 這些是雷達上最強勁的股市。

Related articles

.jpg?height=420)

此處提供的材料並未按照旨在促進投資研究獨立性的法律要求準備,因此被視為市場溝通之用途。雖然在傳播投資研究之前不受任何禁止交易的限製,但我們不會在將其提供給我們的客戶之前尋求利用任何優勢。

Pepperstone 並不表示此處提供的材料是準確、最新或完整的,因此不應依賴於此。該信息,無論是否來自第三方,都不應被視為推薦;或買賣要約;或征求購買或出售任何證券、金融產品或工具的要約;或參與任何特定的交易策略。它沒有考慮讀者的財務狀況或投資目標。我們建議此內容的任何讀者尋求自己的建議。未經 Pepperstone 批準,不得復製或重新分發此信息。