The aim of this is to proactively push inflation (in the US) above its long-held target of 2%. When above this threshold, inflation would then be tolerated on a sustained basis.

This is widely different from years gone by when the Fed would signal rate hikes were coming well before inflation hit 2%.

So, the Fed’s reaction function has essentially changed, which means they will be far slower to hike, even well into the future when the economy is growing above trend and the labour market is strong.

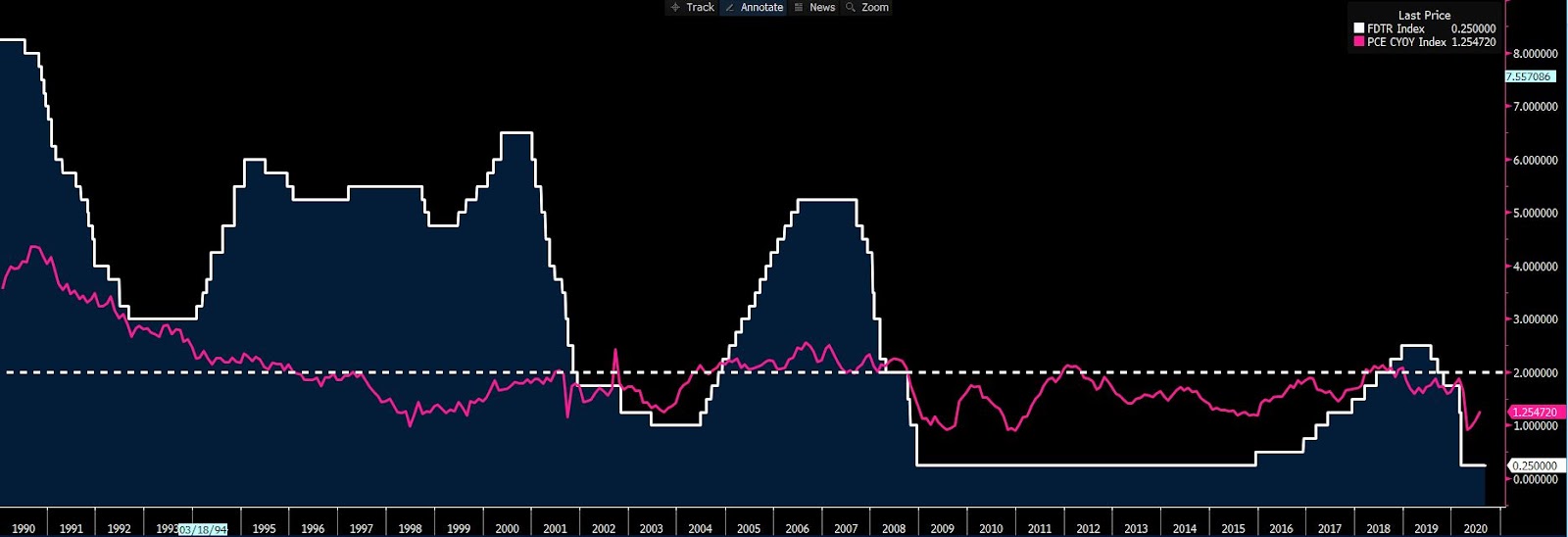

(White - the fed funds rate, pink - core inflation)

(Source: Bloomberg)

The Fed moving to AIT and letting the economy run hot is absolutely the right policy. But, if the Fed’s going to drive inflation to 2%, aside from base effects, we need to know how on earth they’re going to do this.

That’s why next Wednesday’s (Thursday 4am AEST) FOMC meeting is so undeniably critical. There could be fireworks in the market and our clients are getting ready to trade it.

Consider that aside from a brief period in 2006/07, the Fed is going to execute on something they have simply failed to do since 1995.

This is an institution that has failed miserably to meet its inflation forecasts time and time again.

It’s easy to be cynical, but if the Fed is to be seen as credible, gaining the market's respect is key above all else. So, we want answers and they need to come next week. Waiting just won't cut it.

So how do they do it?

The Fed needs to change behaviours: they need to convince the public that prices are going up. This isn’t just by pumping up financial markets and making credit/loan repayments insanely cheap. The public needs to believe everyday items that feed into the inflation calculation are going up. By altering the perception of future prices, it manifests into actual inflation.

This is incredibly difficult, but it’s the only way. Inflation expectations breed inflation. By lifting inflation expectations and putting in measures to keep bond yields anchored, ‘real’ bond yields will move even deeper into the negative, the USD will weaken and asset prices will push higher.

A weaker USD is critical in driving higher inflation. Although a one-way move in the USD will increase talk of currency wars and a race to the bottom, which is why gold is so attractive in this environment.

The Fed would dearly like more stimulus at a fiscal level, but that’s out of their hands. But if they’re going to gain the credibility they crave from the market, they simply must go sooner and bring out the big guns.

If they get it right? We’ll see equities and gold trade higher, with real Treasury yields and the USD lower.

However, if they don’t offer us clarity, urgency and a clear plan, the market will take its pound of flesh and the USD will rally.

If they’re going to do what they have failed to do for so many years, they simply need to make it happen next week and show the world they mean business. Credibility is everything.

Related articles

做好交易准备了吗?

只需少量入金便可随时开始交易。我们简单的申请流程仅需几分钟便可完成申请。

此处提供的材料并未按照旨在促进投资研究独立性的法律要求准备,因此被视为市场沟通之用途。虽然在传播投资研究之前不受任何禁止交易的限制,但我们不会在将其提供给我们的客户之前寻求利用任何优势。

Pepperstone 并不表示此处提供的材料是准确、最新或完整的,因此不应依赖于此。该信息,无论是否来自第三方,都不应被视为推荐;或买卖要约;或征求购买或出售任何证券、金融产品或工具的要约;或参与任何特定的交易策略。它没有考虑读者的财务状况或投资目标。我们建议此内容的任何读者寻求自己的建议。未经 Pepperstone 批准,不得复制或重新分发此信息。